Updated: June 2026 | Reading Time: 17 Minutes

Your dog just got hurt. The vet says he needs surgery. And somewhere in the back of your mind, you’re asking yourself: will my pet insurance actually cover this?

If you’re standing in a veterinary clinic wondering whether your insurance will help cover a $3,000 or $5,000 surgery bill, you’re not alone. Understanding what’s covered before you approve treatment can save both money and unnecessary stress.

That’s not a simple yes or no — and how your policy answers that question will determine whether you’re looking at a $500 bill or a $5,000 one. Here’s what you actually need to know before authorizing that procedure.

Quick Answer Does Pet Insurance Cover Surgery

Yes — pet insurance generally covers surgery, but only under specific conditions. The surgery must be medically necessary, caused by a new accident or illness (not a pre-existing condition), and it must occur after your policy’s waiting period has ended. Reimbursement typically ranges from 70% to 90% of the covered cost, after your deductible.

At a Glance: Surgery Coverage Summary

| Situation | Covered? |

|---|---|

| Emergency surgery after an accident | ✅ Usually yes |

| Surgery for a new illness (cancer, bloat, etc.) | ✅ Usually yes |

| Surgery for a pre-existing condition | ❌ Usually no |

| Surgery during the waiting period | ❌ No |

| Elective surgery (spay/neuter, ear cropping) | ❌ No |

| Hereditary condition surgery (breed-specific) | ⚠️ Depends on plan |

| Orthopedic surgery (CCL/ACL tear) | ⚠️ Often yes, with conditions |

| Prophylactic (preventive) surgery | ❌ Usually no |

| Anesthesia and hospitalization fees | ✅ Covered under most plans |

| Specialist surgeon fees | ✅ Covered under most comprehensive plans |

Surgery is usually covered only if:

✅ It’s medically necessary

✅ It’s not pre-existing

✅ Waiting period is over

✅ Policy is active

✅ Treatment is eligible under your plan

Table of Contents

- What Surgeries Does Pet Insurance Cover?

- What Surgeries Are Not Covered?

- How Much Does Dog Surgery Cost Without Insurance?

- How Does Reimbursement Actually Work?

- Before You Approve Your Dog’s Surgery, Ask Your Insurer These 5 Questions

- The Waiting Period Problem — And Why It Matters More Than You Think

- What Happens If Your Claim Gets Denied?

- Should You Buy Pet Insurance If Your Dog Already Needs Surgery?

- Action Checklist Before Your Dog’s Surgery

- FAQ

What Surgeries Does Pet Insurance Cover?

Most comprehensive (accident and illness) pet insurance plans cover surgery that is medically necessary and caused by a covered condition. That covers a wide range of procedures.

Common surgeries that are typically covered:

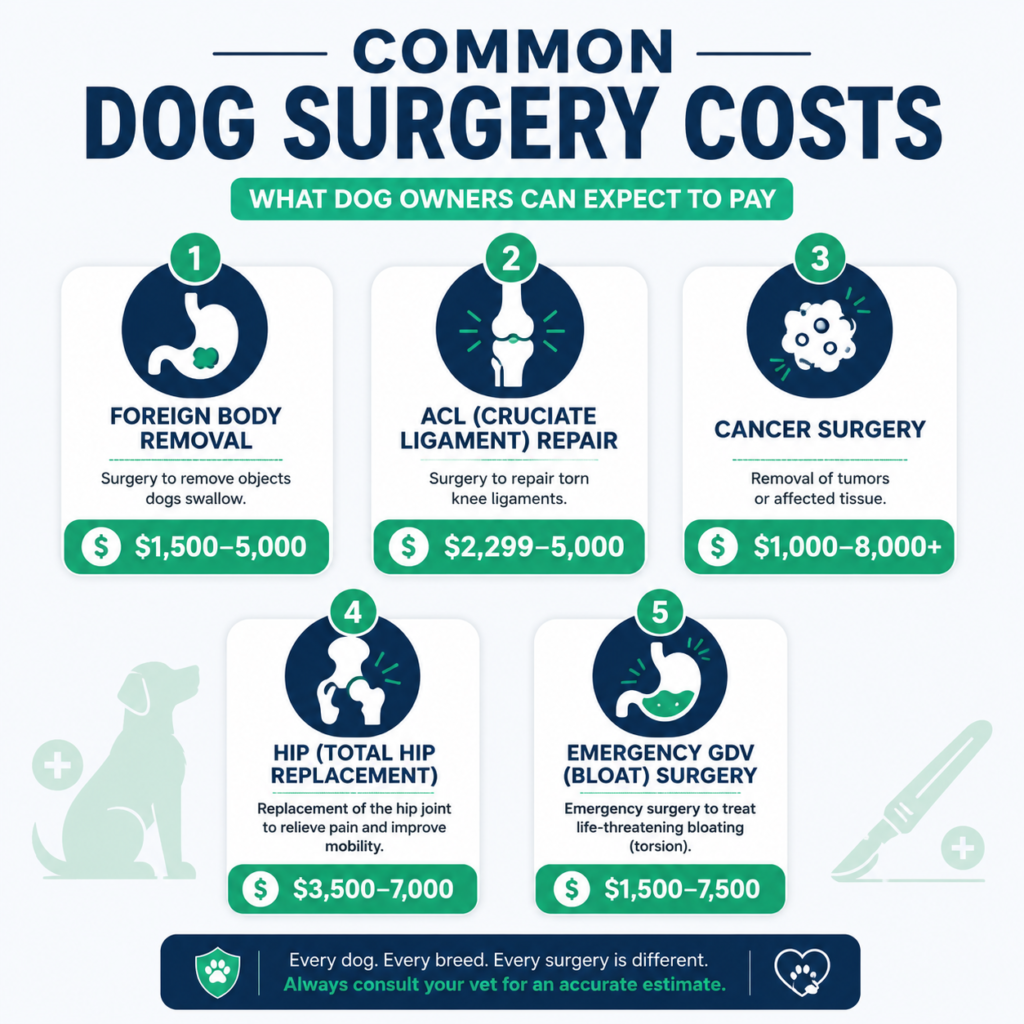

- Foreign body removal — your dog swallowed a sock, a toy, or a corn cob. Surgery to remove it from the intestinal tract costs $1,500–$5,000 and is almost always covered if your policy is active.

- CCL/ACL repair — a torn cranial cruciate ligament is one of the most common surgeries in dogs. Repair averages $2,299–$5,000 per leg depending on procedure type and location.

- Bloat/GDV surgery — gastric dilatation-volvulus is life-threatening. Emergency surgery costs $1,500–$7,500. Covered if no prior symptoms existed.

- Cancer surgery — tumor removal, mass excision, and cancer-related procedures are covered under accident-and-illness plans.

- Fracture repair — broken bones from accidents are typically covered under both accident-only and comprehensive plans.

- Eye surgery — enucleation (eye removal) and other medically necessary eye procedures generally qualify.

- Hip surgery — hip replacement for injury-related hip problems may be covered, though hereditary hip dysplasia has policy-specific nuances.

- Bladder stone removal — averaging around $1,821 for dogs according to CareCredit’s 2024 cost data.

Most plans also cover the costs that come with surgery — anesthesia, hospitalization, post-op medications, and specialist surgeon fees. Those add-on costs matter because they can easily add $500–$2,000 to a single procedure.

Key Takeaway: Comprehensive pet insurance covers most surgeries caused by new accidents and illnesses — including emergency procedures, cancer surgeries, and orthopedic repairs. The key qualifiers are: medically necessary, not pre-existing, and past the waiting period. If all three boxes are checked, you’re likely covered.

What Surgeries Are Not Covered?

This is where dog owners get burned — not because the insurance is dishonest, but because the exclusions aren’t always obvious until you’re filing a claim.

Surgeries that are typically excluded:

Pre-existing conditions. If your dog was limping before you bought the policy, a vet visit documented that limping, and he later needs CCL surgery — that claim will likely be denied. Insurance companies look at your dog’s medical history during underwriting.

Elective and cosmetic procedures. Spaying and neutering, ear cropping, tail docking, and declawing are not covered under standard accident-and-illness plans. Some wellness add-ons cover spay/neuter up to a set limit.

Hereditary and congenital conditions (sometimes). This is tricky. Hip dysplasia in German Shepherds, for example, is a known breed-related issue. Some insurers exclude hereditary conditions outright. Others — like ASPCA Pet Health Insurance’s Complete Coverage plan — do cover them. Always check before enrolling.

Prophylactic surgeries. A vet recommends gastropexy surgery for your Great Dane to prevent bloat before it happens. Most insurers won’t cover this, even if the vet strongly advises it, because it’s preventive rather than reactive.

Breeding-related procedures. C-sections and complications from pregnancy are excluded from standard policies.

Surgeries during the waiting period. If your dog tears her ACL three days after you enrolled, that injury will be considered a pre-existing condition on your new policy. This catches a lot of owners off guard.

How to Quickly Tell If Your Dog’s Surgery May Be Covered

| Question | Yes | No |

|---|---|---|

| Policy active? | Continue | Not covered |

| Waiting period over? | Continue | Likely denied |

| Pre-existing? | Not covered | Continue |

| Medically necessary? | Usually covered | Usually excluded |

| Surgery Type | Typically Covered? | Notes |

|---|---|---|

| Emergency foreign body removal | ✅ Yes | After waiting period |

| CCL/ACL repair | ✅ Yes (usually) | Not if prior limping documented |

| Bloat/GDV surgery | ✅ Yes | Must be new onset |

| Cancer tumor removal | ✅ Yes | Comprehensive plans |

| Hip replacement (injury-caused) | ✅ Yes | Injury context required |

| Hip dysplasia surgery | ⚠️ Plan-dependent | Some exclude hereditary issues |

| Spay/neuter | ❌ No | Wellness add-on may cover |

| Ear cropping | ❌ No | Cosmetic |

| Prophylactic gastropexy | ❌ No | Preventive, not reactive |

| Pre-existing condition surgery | ❌ No | Core exclusion on all policies |

Key Takeaway: The surgeries that get denied most often are pre-existing condition claims and procedures during waiting periods. If your dog has any documented health history — even a routine vet note mentioning a limp — review your policy carefully before assuming a future surgery will be covered.

How Much Does Dog Surgery Cost Without Insurance?

Without coverage, surgery costs can feel impossible. Most dog owners don’t realize how fast a single emergency procedure escalates — especially at a specialty or 24-hour emergency hospital, which typically charges 2–4x what a general practice vet would.

2026 average cost ranges for common dog surgeries:

| Procedure | Average Cost Range |

|---|---|

| Foreign body removal | $1,500 – $5,000 |

| CCL/ACL repair | $2,299 – $5,000 per leg |

| Bloat/GDV emergency surgery | $1,500 – $7,500 |

| Hip replacement (per hip) | $3,500 – $7,000 |

| Bladder stone removal | $800 – $2,500 |

| Cancer/tumor removal | $1,000 – $8,000+ |

| Fracture repair | $1,000 – $5,000 |

| Eye removal (enucleation) | $600 – $1,000 |

| Cataract surgery | $2,700 – $4,500 |

| Limb amputation | $700 – $1,000 |

These are national averages. If you’re in California, New York, or another high cost-of-living state, expect the upper end of those ranges. Rural areas and general practice vets tend to be lower.

➡ Related Guide: Why Was My Pet Insurance Claim Denied? 5 Common Reasons (And How to Fix Them)

Emergency vet visits alone — before surgery even begins — run $150–$250 just for the initial exam. Add diagnostics (X-rays: $100–$400, bloodwork: $75–$200, ultrasound: $300–$600), and you can easily spend $800–$1,500 before anyone picks up a scalpel.

➡ Related Guide: Emergency Vet vs Regular Vet Cost: Why Emergency Care Costs So Much More

According to data from AVMA and NAPHIA, emergency surgery can run $2,000–$5,000+ for most procedures, and complex cases involving ICU stays or specialists can exceed $10,000.

Only about 20% of dog owners can comfortably afford a $5,000 emergency vet bill out of pocket. That means for the other 80%, the cost question isn’t abstract — it determines what care their dog actually receives.

Key Takeaway: Even a routine dog surgery at an emergency clinic can reach $3,000–$5,000 after diagnostics and hospitalization. Without insurance or a financing plan already in place, most owners face a difficult financial decision in a high-stress moment. Knowing the numbers ahead of time gives you options.

How Does Reimbursement Actually Work?

Pet insurance doesn’t work like human health insurance. Your vet doesn’t bill the insurer directly — you pay the full cost upfront, then submit a claim and wait for reimbursement. This catches a lot of dog owners off guard mid-emergency.

The three numbers that determine your actual reimbursement:

1. Reimbursement rate. Most plans offer 70%, 80%, or 90%. This is the percentage of eligible costs the insurer pays back after your deductible is met.

2. Annual deductible. This is what you pay out of pocket before reimbursement kicks in. Options typically range from $100 to $1,000. A higher deductible lowers your monthly premium.

3. Annual coverage limit. Some plans cap total annual reimbursement at $5,000, $10,000, or unlimited. If your dog has a $7,000 surgery on a $5,000 limit plan, you absorb the difference.

➡ Related Guide: Pet Insurance for Dogs in the USA: How It Works (2026)

A realistic example:

Your dog needs emergency surgery for a foreign body obstruction. Total bill: $4,200.

- Annual deductible: $250 (already met earlier in the year)

- Reimbursement rate: 80%

- Eligible costs after deductible: $4,200

- Insurer pays: $3,360

- Your out-of-pocket: $840

Mini table.

| Total Bill | $4,200 |

|---|---|

| Deductible | $250 |

| Eligible | $3,950 |

| 80% Paid | $3,160 |

| You Pay | $1,040 |

That’s a meaningful difference. Without insurance, you’d owe the full $4,200 — and you’d need it before leaving the clinic.

Important: You still pay the vet upfront and wait for reimbursement, which typically takes 5–15 business days depending on the insurer. Some insurers now offer direct payment to vets or expedited claims — worth asking before a crisis happens.

Key Takeaway: Reimbursement rates of 80–90% sound great but your actual savings depend on your deductible, annual limit, and whether the procedure is fully covered. Run the numbers on your specific policy before an emergency — not during one.

Before You Approve Your Dog’s Surgery, Ask Your Insurer These 5 Questions

Before you authorize surgery, take five minutes to call your pet insurance provider. The answers you get can prevent unexpected bills, denied claims, and reimbursement delays. Even if your policy is active, it’s worth confirming exactly how your coverage applies to your dog’s specific procedure.

| Ask Your Insurer | Why It Matters |

|---|---|

| Is this surgery covered? | Confirms eligibility before treatment |

| Any exclusions? | Helps avoid denied claims |

| Is pre-authorization required? | Prevents claim delays |

| Has the waiting period ended? | Avoids unexpected exclusions |

| What’s my reimbursement limit? | Helps estimate your out-of-pocket cost |

The Waiting Period Problem — And Why It Matters More Than You Think

This is the #1 reason pet insurance claims get denied for surgery.

Every pet insurance policy has a waiting period — a gap between when you enroll and when coverage actually begins. During that window, any condition that develops is typically classified as a pre-existing condition and excluded from future claims.

Standard waiting periods:

| Coverage Type | Typical Waiting Period |

|---|---|

| Accident coverage | 24–48 hours |

| Illness coverage | 14 days |

| Orthopedic conditions (CCL, hip) | 6 months (some insurers) |

| Cruciate ligament injuries | 6–12 months (varies by insurer) |

That last one matters enormously. Some insurers — particularly for orthopedic surgeries like CCL repair — impose waiting periods of 6 to 12 months specifically for those procedures. So a dog owner who buys insurance on Monday, and whose dog tears a CCL on the following Saturday, will face a denied claim — even though they technically had coverage.

➡ Related Guide: Pet Insurance Waiting Period: How Long Before Coverage Starts?

What this means practically:

- Buy insurance before your dog is injured, not after.

- Don’t assume “accident coverage” starts on day one for all accident types.

- If you have a high-risk breed (Labrador, Golden Retriever, Rottweiler) that’s prone to CCL injuries — check the orthopedic waiting period specifically before you enroll.

Key Takeaway: Waiting periods are the fine print that matters most. For orthopedic surgeries especially, some policies won’t reimburse anything for the first 6–12 months. Enroll early, read the orthopedic clause specifically, and don’t wait until your dog is limping.

What Happens If Your Claim Gets Denied?

A denial doesn’t always mean the end of the road. Understanding why claims get denied — and what you can do about it — is something most insurers don’t make easy to find.

Common reasons surgery claims are denied:

- The condition existed before enrollment (pre-existing)

- Surgery occurred during the waiting period

- The procedure is classified as elective

- Insufficient medical records to prove the condition was new

- The annual coverage limit was already reached

- Procedure excluded under a hereditary condition clause

What you can do:

- Request the denial reason in writing. Insurers are required to provide a specific reason.

- Appeal with supporting documentation. If your vet can document that the condition was new and unrelated to prior history, an appeal can succeed.

- Ask your vet for a letter. A veterinarian’s statement clarifying the onset and nature of the condition carries significant weight in appeals.

- File a complaint with your state’s insurance commissioner if you believe the denial violates your policy terms. Pet insurance is regulated at the state level.

- Review NAPHIA standards. The North American Pet Health Insurance Association publishes consumer guides on insurer obligations and fair claims practices.

If the denial holds and you’re facing a large bill, CareCredit and Scratchpay offer veterinary financing that can spread the cost over 6–24 months. Some emergency vets also accept payment plans directly, though these vary widely by practice.

Key Takeaway: A denied claim is worth appealing — especially when supported by veterinary documentation showing the condition was newly developed. Don’t accept the first denial as final. And always keep full records of your dog’s vet visits; a complete medical history is your best defense in a dispute.

Should You Buy Pet Insurance If Your Dog Already Needs Surgery?

This is a real situation. Your dog has been limping for a few days. You haven’t bought insurance yet. You’re wondering if it’s too late.

The honest answer: For that specific injury — probably yes, it’s too late. Any condition showing symptoms before the policy start date will almost certainly be classified as pre-existing. If your dog needs CCL surgery and you enroll today, that surgery will not be covered.

➡ Related Guide: Best Vet Payment Plans in the USA (2026): CareCredit vs Scratchpay

But here’s the nuance:

Buying insurance now still makes sense for everything else your dog might need. Dogs who’ve had one orthopedic injury often have another — but on a different leg, which may be covered after the waiting period on a new policy. Future illnesses, accidents unrelated to the current injury, cancer, dental disease, and other conditions would all be eligible.

Should You Buy Pet Insurance Now?

| Situation | Makes Sense? | Why |

|---|---|---|

| Healthy puppy or young dog | ✅ Absolutely | Lock in lower premiums, no pre-existing exclusions |

| Adult dog, no major health issues | ✅ Yes | Before problems develop |

| Dog with one prior injury, otherwise healthy | ✅ Yes | Covers everything else; future injuries on other limbs |

| Dog with chronic illness needing ongoing surgery | ⚠️ Maybe | That condition excluded; evaluate what else might be covered |

| Dog who needs surgery right now | ❌ For this surgery | Waiting period and pre-existing rules will block coverage for current issue |

Key Takeaway: Buying insurance after your dog shows symptoms won’t help for that condition. But it can still protect you from the next emergency — and for a healthy dog, early enrollment is one of the best financial decisions you can make as an owner.

Action Checklist Before Your Dog’s Surgery

Use this before authorizing any procedure:

- Confirm your pet insurance policy is active and past all applicable waiting periods

- Call your insurer before surgery to ask about pre-authorization (some companies offer this)

- Request an itemized estimate from your vet — not just a total figure

- Ask the vet to document that the condition is new and not pre-existing

- Check your annual coverage limit to confirm you haven’t hit the cap this year

- Know your deductible status — have you already met it this policy year?

- Confirm anesthesia, hospitalization, and specialist fees are covered under your plan

- If uninsured, ask about CareCredit or Scratchpay financing at the clinic

- Keep all invoices and medical records — you’ll need them for the claim

- Submit your claim promptly after surgery; most insurers have submission deadlines

External Authority Sources

- NAPHIA (North American Pet Health Insurance Association)

- CareCredit Veterinary Cost Guide

- AVMA (American Veterinary Medical Association)

- ASPCA Animal Poison Control Center

Frequently Asked Questions

Does pet insurance cover surgery on the same day you buy a policy?

No. Pet insurance doesn’t provide immediate coverage for surgery. Most policies include waiting periods for accidents, illnesses, and sometimes orthopedic conditions. If your dog needs surgery before those waiting periods end, the claim is usually denied. Buying coverage before any health problem develops gives you the best chance of being covered.

Does pet insurance cover emergency surgery?

Yes. Most accident-and-illness pet insurance plans cover emergency surgery caused by a new accident or illness, provided the condition isn’t pre-existing and all waiting periods have ended. Emergency exam fees, diagnostics, and hospitalization may also be covered depending on your policy.

Does pet insurance cover ACL or CCL surgery in dogs?

Usually yes, but many insurers apply a longer waiting period for orthopedic conditions. If your dog tears a cruciate ligament before coverage begins or during the waiting period, the surgery is typically excluded. Always check your insurer’s orthopedic policy before enrolling.

Can I get pet insurance right before my dog’s surgery?

You can enroll at any time, but the current surgery usually won’t be covered. Conditions that appear before your policy starts or during the waiting period are generally treated as pre-existing and excluded from reimbursement.

What happens if my dog needs surgery I can’t afford?

If your dog’s surgery isn’t covered or you don’t have insurance, ask your veterinarian about payment options before delaying treatment. Many clinics accept financing through CareCredit or Scratchpay, and some nonprofit organizations provide emergency veterinary assistance for eligible pet owners.

Does pet insurance cover surgery for hereditary conditions?

It depends on the insurer and your policy. Many plans cover hereditary conditions if symptoms appear after coverage begins, while others apply exclusions or additional requirements. If your dog’s breed is prone to hereditary health problems, review the policy details before enrolling.

What You Should Do Next

If your dog is healthy right now — this is the moment to get coverage in place. Not after a diagnosis. Not after a limp starts. Premiums are lower for young, healthy dogs, and you avoid the pre-existing condition trap entirely.

If your dog already needs surgery — focus on what’s in front of you. Call your insurer today if you have coverage and ask directly whether the procedure is eligible. Get the answer in writing. If you’re uninsured, ask the emergency clinic about CareCredit or Scratchpay before you assume you have no options.

Pet insurance covers a lot — but the owners who benefit most are the ones who understood the policy before they needed it.

Disclaimer

This article is for informational and educational purposes only. Cost data reflects 2026 national averages from NAPHIA, Insurify, and MetLife Pet Insurance and will vary based on your dog’s age, breed, location, and the specific plan you choose. PetInsurePrime does not sell pet insurance and receives no compensation from any insurance provider. Always compare multiple quotes and read your policy documents carefully before enrolling.

PetInsurePrime | Independent • Research-Based | Helping US dog owners understand real vet costs and coverage options — without the sales pressure.