Updated: June 2026 | Reading Time: 14 Minutes | Reviewed Sources NAPHIA , AVMA , NAIC

Imagine finally getting help for your dog’s surgery—only to receive an email saying your claim was denied because the condition was “pre-existing.” It’s one of the biggest frustrations pet owners face, especially when they thought they had done everything right. The problem is that “pre-existing condition” doesn’t always mean your dog was formally diagnosed. In many cases, a symptom noted in an old veterinary record is enough for an insurer to deny coverage. This guide explains exactly how these rules work, which conditions may still become eligible for coverage, and how you can avoid costly surprises before buying a policy. If you’re still learning the basics of how coverage works, read our complete guide to Pet Insurance for Dogs in the USA: How It Works (2026) first.

Key Takeaways

✔ Most pet insurance plans exclude pre-existing conditions.

✔ Symptoms without a formal diagnosis may still count as pre-existing.

✔ Curable conditions may become eligible after a symptom-free period.

✔ Chronic conditions are usually permanently excluded under standard policies.

✔ Buying insurance before health problems appear gives the best protection.

Quick Answer Does Pet Insurance Cover Pre-Existing Conditions

Most pet insurance plans do not cover pre-existing conditions. However, some insurers may cover curable conditions after your pet has remained symptom-free for 180 days to 12 months. Currently, AKC Pet Insurance is one of the few providers that may cover certain incurable pre-existing conditions after 365 days of continuous coverage, subject to policy terms.

What Counts as a Pre-Existing Condition?

| Condition Type | Usually Covered | Notes |

|---|---|---|

| Curable | Sometimes | 180–365 days |

| Chronic | No | Usually excluded |

| New illness | Yes | After waiting period |

| Accident | Yes | If unrelated |

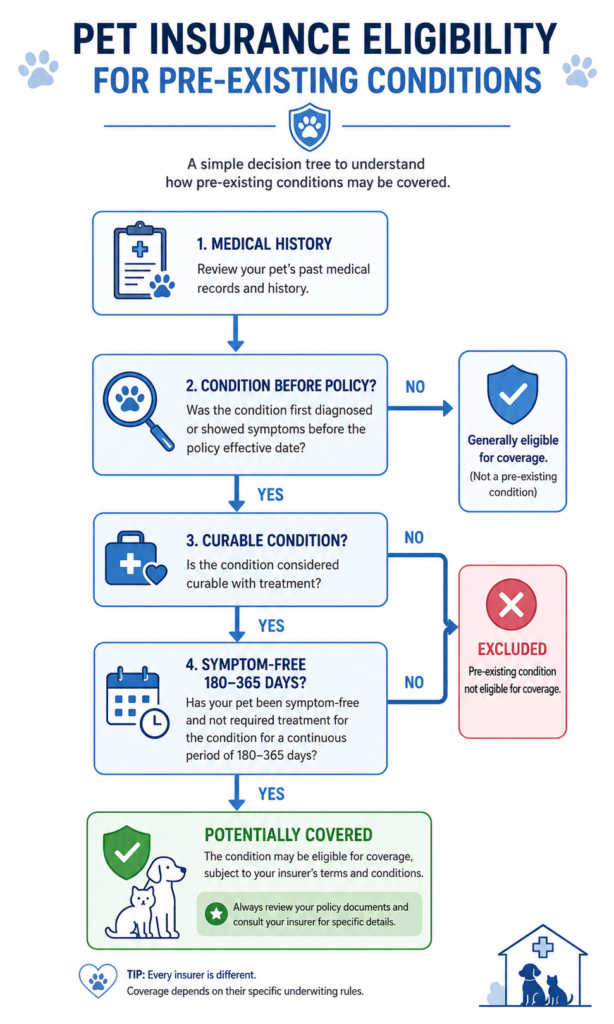

In simple terms, a pre-existing condition is any illness, injury, or symptom your pet showed before your insurance coverage officially began. Different insurers define this slightly differently, but almost all review your pet’s medical history when evaluating claims

A pre-existing condition is any condition your pet has shown signs or symptoms of, has been diagnosed with, or has been treated for before the insurance policy’s effective date. Lemonade

That definition is broader than most owners expect — and it creates some outcomes that feel deeply unfair.

Here’s the part that catches people off guard: previously documented symptoms can be considered pre-existing conditions even without a formal diagnosis. If those symptoms reappear after you enroll your pet in pet insurance, treatments related to those symptoms may not be covered. GoodRx

So if your dog was limping at a checkup two years ago and your vet noted it in the records — even casually, even without a diagnosis — an insurer reviewing those records later may classify a knee injury claim as pre-existing. Even in the absence of a diagnosis, symptoms documented before a pet is covered can be treated as pre-existing. PetMD

Many pet parents assume only confirmed diagnoses count, but insurers usually look at the full medical record — including exam notes, test results, past treatments, and even recommendations for follow-up care. PetPlace

This is why the timing of enrollment matters so much. The earlier you insure a dog, the cleaner their medical history tends to be. Many denied claims begin with misunderstanding how coverage starts. Our guide on Why Was My Pet Insurance Claim Denied? explains the most common reasons insurers reject claims.

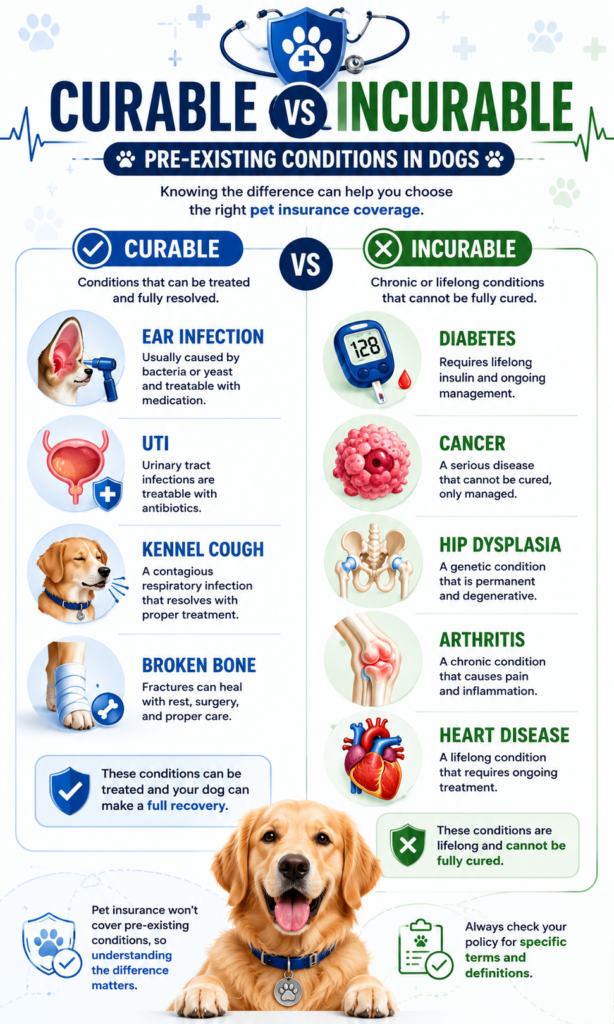

Curable vs Incurable: The Distinction That Changes Everything

Not all pre-existing conditions are treated the same. The single most important thing to understand is whether a condition is classified as curable or incurable — because that determines whether it might ever be covered down the road.

Curable Pre-Existing Conditions

Curable conditions are defined as any medical condition or illness that your pet has been treated for and cured of. Most insurance companies require 180 symptom-free days to consider a condition cured, while some require a full year. PetMD

Curable pre-existing conditions are usually defined as illnesses or injuries that have been fully treated and have not recurred for a certain period, often 6 to 12 months. Each provider has a different list of conditions it considers curable. CNBC

Common examples of curable conditions:

- Ear infections

- Urinary tract infections

- Kennel cough

- Vomiting and diarrhea (non-chronic)

- Broken bones

- Upper respiratory infections

- Sprains

If your dog had an ear infection before enrollment, resolved it completely, and stayed symptom-free for 180 days — many insurers will remove that exclusion from your policy and cover future ear infections.

Incurable Pre-Existing Conditions

Incurable pre-existing conditions are those your pet will have for a lifetime. These include chronic diseases or conditions with no known cure. Insurance policies typically don’t cover these if they’re present before the policy starts or during a waiting period. nerdwallet

Common examples of incurable conditions:

- Allergies

- Diabetes

- Cancer

- Arthritis

- Chronic kidney disease

- Hip dysplasia

- Epilepsy

- Heart disease

- Hypothyroidism

All incurable or chronic conditions diagnosed before enrollment are permanently excluded under standard policies. No amount of symptom-free time will change that — with one narrow exception covered below. Pet-insurance-hub

| Curable | Incurable |

|---|---|

| Ear infection | Diabetes |

| UTI | Cancer |

| Kennel cough | Arthritis |

| Broken bone | Hip dysplasia |

If your insurer has already denied coverage because of a pre-existing condition, don’t assume the decision is final. Learn how to challenge the decision in our guide on How to Appeal a Denied Pet Insurance Claim.

The Bilateral Condition Trap

This is one of the most misunderstood and most painful parts of pet insurance policy language. Many owners only discover it after a claim gets denied.

A bilateral condition is any health issue that can affect both sides of the body — knees, hips, elbows, eyes.

Most insurers don’t cover bilateral conditions once your pet has symptoms or a diagnosis on one side of the body. For example, if your dog has hip dysplasia on its left side — even after surgery and recovery — most insurers won’t cover care for hip dysplasia in either hip, because it’s a bilateral condition. Insurify

If your pet experiences a torn ligament on one knee, the other knee would be excluded for the same condition — even if that injury occurs after the policy’s coverage begins. GoodRx

Common bilateral conditions that trigger this exclusion:

- Hip dysplasia

- Cruciate ligament tears (CCL/ACL)

- Elbow dysplasia

- Cataracts

- Glaucoma

Some bilateral conditions may be considered curable and can eventually be covered. For example, if your dog had an ear infection in the right ear before enrollment but develops a left ear infection after the policy kicks in, the insurance company will likely cover it — as long as your dog was symptom-free for 180 days after the first infection. PetMD

Orthopedic conditions like ACL tears and hip dysplasia often lead to expensive procedures. See our breakdown of Dog Surgery Cost in the USA to understand the financial impact.

What Insurers Actually Look At

When you file a claim, insurers don’t just review the treatment you’re billing for. They go back through your dog’s complete medical history.

Common Mistakes Pet Owners Make

- Waiting until the pet gets sick before buying insurance.

- Assuming only diagnosed illnesses count.

- Forgetting about old vet records.

- Letting an active policy lapse.

- Not checking bilateral condition rules.

- Switching insurers without understanding new exclusions.

This review includes assessing past treatments and documented signs, symptoms, or concerns your pet has experienced — even if untreated or undiagnosed. If your pet showed signs of vomiting and upset stomach before the policy’s effective date and was later diagnosed with gastroenteritis, the gastroenteritis would be considered pre-existing and related tests and treatments wouldn’t be covered. Companionpetmagazine

Read more Emergency Vet Costs in the USA (2026)

Pet insurance companies employ teams of veterinary specialists trained to review medical records and determine if a pet has any pre-existing medical conditions. They look for patterns — a symptom noted at one visit, a follow-up question logged at another — even when no formal diagnosis was made at the time. Insuranceopedia

During Claim Review, Insurers May Check:

- Vet records

- Symptoms

- Exam notes

- Diagnostic reports

- Previous treatments

- Follow-up recommendations

What this means practically: your dog’s vet records are the document that either supports or defeats your claim. Before you enroll in any policy, it’s worth requesting those records yourself so you know exactly what’s documented.

If your claim is denied after medical records are reviewed, our step-by-step Pet Insurance Claim Appeal Guide explains exactly what documentation insurers usually request.

The Only Real Exception for Incurable Conditions

AKC Pet Insurance is currently the only major brand that offers coverage for both curable and incurable pre-existing conditions after 365 days of continuous coverage. AKC Pet Insurance

AKC Pet Insurance is the only pet insurance company that covers incurable, chronic pre-existing conditions like diabetes, cancer, and hip dysplasia — but you’ll need to have your policy active for 12 months before the benefit applies. CNBC

This is meaningful for owners whose dogs already have chronic conditions and who want some path to future coverage. It’s not unlimited protection — there are specific terms and conditions — but it’s the only option in the market that even offers it for truly incurable conditions.

For curable conditions, several other major insurers offer reconsideration after a symptom-free period:

| Company | Curable | Incurable |

|---|---|---|

| Pets Best | 180 Days | No |

| ASPCA | 180 Days | No |

| Lemonade | 12 Months | No |

| Spot | 180 Days | No |

| AKC | 365 Days | Yes |

Every insurer defines “curable” differently. Always verify in the actual policy document.

Important: Coverage for eligible pre-existing conditions under AKC Pet Insurance depends on state availability, continuous coverage, and specific policy terms. Always review the latest policy wording before enrolling.

How Narrow or Broad the Exclusion Gets: It Depends on the Insurer

Not all exclusions are created equal — and the scope matters.

Some insurers apply exclusions per-condition rather than system-wide. For example, if your dog has left hip dysplasia, some providers exclude left hip dysplasia specifically — not all musculoskeletal conditions, and not necessarily the right hip unless bilateral dysplasia was documented. This narrower exclusion scope is a meaningful advantage over providers who exclude entire body systems. Pet-insurance-hub

Before committing to a policy, it’s worth calling the insurer directly and asking: “If my dog has [specific condition], what exactly would be excluded — just that condition, or everything related to that body system?” The answer tells you a lot about how that company actually handles claims.

Does Pet Insurance Still Make Sense If Your Dog Has a Pre-Existing Condition?

Yes — and here’s why.

If your pet already has a pre-existing condition that would be excluded from coverage, insurance can still be worthwhile. Your pet can still have coverage for new injuries and illnesses that develop after enrollment. MetLife Pet Insurance

A dog with allergies that develop cancer. A dog with hip dysplasia that gets hit by a car. A dog with diabetes that needs emergency surgery for a blockage. None of those new events are related to the pre-existing condition — and all of them would typically be covered under a standard policy.

The pre-existing condition exclusion means that specific condition won’t be covered. It doesn’t make insurance worthless.

If your pet insurance policy lapses, anything your pet has been diagnosed with up until that point can be considered a pre-existing condition and excluded from coverage when you re-enroll. Keep your policy active by paying your premiums on time and renewing before expiration. This is one of the biggest mistakes owners make — letting coverage lapse thinking they’ll restart it later. Each gap in coverage can lock in new exclusions. nerdwallet

What to Do Before You Buy

Get your dog’s full vet records first. You need to know exactly what’s documented, because a symptom you barely remember from two years ago can still matter to an insurer reviewing those records. PetPlace

Call the insurer and ask directly. Ask prospective insurers how they would classify past issues. They may not give a guaranteed final coverage decision in advance, but they can explain how their rules work and what records they require. PetPlace

Enroll young when possible. The earlier you insure a dog, the fewer documented conditions exist to trigger exclusions. A puppy enrolled before their first wellness exam has the cleanest possible record.

Read the bilateral condition language carefully. If your dog has had any orthopedic issue on one side of the body, find out exactly how the insurer handles the other side before you buy.

Don’t let coverage lapse. Once you have a policy, keep it active. The protections you have today can disappear if coverage breaks.

Frequently Asked Questions (FAQ)

Does pet insurance cover pre-existing conditions?

In most cases, no. Standard pet insurance policies do not cover illnesses or injuries that existed before your policy started or during the waiting period. A condition may be considered pre-existing even if your pet was never formally diagnosed, as insurers often review symptoms, veterinary notes, and medical history when evaluating claims. Some companies may reconsider curable pre-existing conditions after your pet has remained symptom-free for a specified period, typically 180 days to 12 months, depending on the insurer and policy.

What if my dog was never officially diagnosed but had symptoms noted by a veterinarian?

A formal diagnosis isn’t always required. If your veterinarian documented symptoms such as limping, chronic itching, vomiting, or recurring ear infections before your policy became effective, insurers may classify future treatment for the same condition as pre-existing. That’s why reviewing your pet’s medical records before purchasing insurance is so important.

Can a pre-existing condition ever become covered?

Sometimes. Many insurers distinguish between curable and incurable pre-existing conditions. Curable conditions, such as certain infections or minor injuries, may become eligible for future coverage after your pet has remained symptom-free for a required period. Chronic or lifelong conditions, however, are generally excluded under standard policies.

What are bilateral conditions and why do they matter?

A bilateral condition affects paired body parts, such as the hips, knees, elbows, or eyes. If your pet develops a condition on one side before enrolling, many insurers also exclude the same condition on the opposite side because it’s considered medically related. This rule commonly affects hip dysplasia and cruciate ligament (ACL/CCL) injuries.

Will pet insurance cover hereditary or congenital conditions?

Often, yes—but timing matters. Many accident and illness plans cover hereditary or congenital conditions only if your pet showed no symptoms before enrollment and after any applicable waiting period. If symptoms appeared before coverage began, the condition may be treated as pre-existing and excluded.

Is there any pet insurance that covers incurable pre-existing conditions?

Currently, AKC Pet Insurance is one of the few providers that offers coverage for eligible curable and incurable pre-existing conditions after 365 consecutive days of continuous coverage, subject to state availability and policy terms. Always review the latest policy details before enrolling because eligibility requirements can vary.

What happens if I switch pet insurance companies?

Switching insurers can create new coverage limitations. Your new provider will evaluate your pet’s complete medical history from the beginning, and conditions that developed under your previous insurer may now be treated as pre-existing. Before changing providers, compare benefits carefully and confirm how existing medical conditions will be handled.

Is pet insurance still worth buying if my dog already has a pre-existing condition?

Yes, in many situations it is. Although your existing condition may be excluded, your policy can still help pay for future accidents, unrelated illnesses, emergency surgeries, cancer treatment, or other new medical problems that occur after enrollment and once waiting periods are satisfied. Insurance can still provide significant financial protection against unexpected veterinary expenses.

How can I reduce the risk of a claim being denied because of a pre-existing condition?

The best approach is to enroll your pet while they’re young and healthy, keep continuous coverage without allowing your policy to lapse, maintain complete veterinary records, and carefully read the insurer’s policy regarding waiting periods, exclusions, and bilateral conditions before purchasing coverage.

Suggested Schema Questions

- Does pet insurance cover pre-existing conditions?

- What counts as a pre-existing condition for pet insurance?

- Can a pre-existing condition be covered by pet insurance later?

- What is a bilateral condition in pet insurance?

- Which pet insurance covers incurable pre-existing conditions?

- What happens to pet insurance if my dog already has a health condition?

- Can symptoms without a diagnosis count as a pre-existing condition?

Final Thoughts

While pre-existing condition rules can seem frustrating, they don’t make pet insurance useless. Most policies still protect your dog against future accidents and illnesses that aren’t related to existing medical problems. Understanding your dog’s medical history, comparing policy wording carefully, and enrolling before health issues appear can make a significant difference in the coverage you receive.

Disclaimer:

This article is for informational and educational purposes only. Cost data reflects 2026 national averages from NAPHIA, Insurify, and MetLife Pet Insurance and will vary based on your dog’s age, breed, location, and the specific plan you choose. PetInsurePrime does not sell pet insurance and receives no compensation from any insurance provider. Always compare multiple quotes and read your policy documents carefully before enrolling.

PetInsurePrime | Independent • Research-Based | Helping US dog owners understand real vet costs and coverage options — without the sales pressure.