Updated: June 2026 | Reading Time: 18 Minutes

Imagine opening a $4,800 veterinary bill only to learn your pet insurance won’t pay a single dollar. For many dog owners, that shock doesn’t happen because they skipped insurance—it happens because they misunderstood what their policy actually excludes.

Most accident-and-illness pet insurance plans cover unexpected injuries and illnesses, but they also contain important exclusions. Pre-existing conditions, routine care, pregnancy, grooming, and several other expenses are commonly left out. Understanding these exclusions before you buy a policy can help you avoid denied claims and unexpected out-of-pocket costs.

If you’re completely new to pet insurance, start with our guide explaining Pet Insurance for Dogs in the USA: How It Works before learning about policy exclusions.

In this guide, you’ll learn exactly what pet insurance usually doesn’t cover, why those exclusions exist, which exclusions vary by insurer, and how to choose a policy that best fits your dog’s needs.

Quick Answer What Doesn’t Pet Insurance Cover?

| Standard Pet Insurance Usually DOES NOT Cover | May Be Covered by Some Plans or Add-ons |

|---|---|

| Pre-existing conditions | Dental illness |

| Routine wellness care | Alternative therapies |

| Grooming | Exam fees |

| Pregnancy & breeding | Prescription food (limited cases) |

| Cosmetic procedures | Behavioral therapy |

| Liability claims | Wellness services |

Table of Content

What Doesn’t Pet Insurance Cover?

- Pre-existing Conditions

- Routine Care

- Dental Coverage

- Grooming

- Cosmetic Procedures

- Pregnancy

- Behavioral Conditions

- Experimental Treatments

- Non-Veterinary Costs

- Liability

- Age Restrictions

- Coverage That Varies

- How to Avoid Claim Denials

- FAQ

Pre-Existing Conditions

This is the biggest exclusion in the industry and the one that generates the most claim denials.

Almost every standard policy excludes any condition your dog showed signs of, was diagnosed with, or was treated for before the policy’s effective date — including during the waiting period. This applies whether the condition was formally diagnosed or just noted as a symptom in a vet record.

There’s an important distinction worth knowing: some insurers treat curable pre-existing conditions differently from incurable ones. Conditions like ear infections or UTIs can sometimes be reconsidered after 180 days symptom-free. Chronic conditions — hip dysplasia, allergies, diabetes, cancer — stay excluded permanently under most standard policies.

The only major insurer that offers any path to coverage for incurable pre-existing conditions is AKC Pet Insurance, and that requires 365 consecutive days of active coverage before the benefit applies.

If your dog already has a known health issue, pre-existing condition exclusions are the first thing to understand before choosing a policy. A full breakdown of how this exclusion works — including the bilateral condition trap — is covered in the pre-existing conditions guide linked below.

Read more.. How to Appeal a Denied Pet Insurance Claim: Step-by-Step Guide to Improve Your Chances

Quick Take

❌ Usually Not Covered

- Ear cropping

- Tail docking

- Cosmetic dental procedures

- Preventive gastropexy

- Elective surgeries performed for convenience

⚠️ May Be Covered

- Procedures that become medically necessary because of an accident, illness, or emergency.

Pet insurance is designed to pay for medically necessary treatment—not elective or cosmetic procedures. If a procedure could fall into either category, ask your insurer for written confirmation before scheduling it.

Routine and Preventive Care

Standard accident-and-illness policies do not cover the routine care your dog needs to stay healthy year-round. That means:

- Annual wellness exams

- Vaccinations (rabies, DHPP, Bordetella, etc.)

- Flea, tick, and heartworm prevention

- Routine deworming

- Spaying and neutering

- Nail trims

- Anal gland expression

- Routine bloodwork and urinalysis

These services aren’t covered because they’re predictable and planned — the opposite of the unexpected accidents and illnesses that insurance is designed for.

The add-on option: Most major insurers offer wellness or preventive care riders you can attach to your base policy for an additional monthly premium. These cover routine items on a scheduled reimbursement basis — a fixed dollar amount per service per year, not a percentage of the actual bill. Whether the math works in your favor depends on how often you use those services. If your dog is young and healthy and visits the vet only for annual exams, a wellness add-on may cost more than it returns. For dogs that need regular preventive care or are in the puppy stage with frequent vaccine visits, it often makes sense.

Routine wellness care is almost never covered under standard accident-and-illness policies. If preventive care matters to you, compare wellness add-ons before choosing a plan.

Dental Disease and Cleanings

Dental coverage is one of the most misunderstood parts of pet insurance—and one of the most expensive surprises for dog owners.

Many people assume that if a veterinarian recommends a dental procedure, their insurance will automatically reimburse the cost. In reality, coverage depends on why the treatment is needed. Most accident-and-illness plans distinguish between accidental dental injuries and dental diseases, while routine dental care is almost always excluded unless you purchase an optional wellness plan. Coverage rules also vary by insurer, making it essential to review your policy before enrolling.

Read more…Dog Surgery Cost in the USA: Real Prices

What Most Pet Insurance Plans Cover

- Broken or fractured teeth caused by an accident

- Tooth extractions resulting from accidental injuries

- Emergency oral surgery after trauma

- Diagnostic X-rays related to a covered dental injury

- Medications prescribed after a covered dental accident

What Most Pet Insurance Plans Don’t Cover

- Routine dental cleanings

- Periodontal (gum) disease

- Tooth decay caused by long-term dental disease

- Cosmetic dental procedures

- Orthodontic treatments

- Pre-existing dental conditions

| Dental Treatment | Usually Covered? |

|---|---|

| Broken tooth caused by an accident | ✅ Usually Yes |

| Emergency tooth extraction (accident) | ✅ Usually Yes |

| Routine dental cleaning | ❌ No |

| Periodontal disease | ⚠️ Depends on the insurer |

| Tooth extraction due to dental disease | ⚠️ Depends on the policy |

| Cosmetic dental procedures | ❌ No |

| Orthodontic treatment | ❌ No |

One of the biggest reasons pet insurance claims are denied is that owners don’t realize dental accidents and dental diseases are treated differently. A broken tooth caused by trauma is often eligible for reimbursement under accident-and-illness coverage. However, periodontal disease, gingivitis, and other dental illnesses may only be covered by certain insurers or may require additional coverage, while routine cleanings are generally available only through optional wellness plans. Always read the dental exclusions section of your policy before enrolling.

Quick Take

✅ Usually Covered

- Broken teeth caused by accidents

- Trauma-related dental surgery

- Diagnostic imaging after a covered accident

⚠️ Coverage Varies

- Periodontal disease

- Dental infections

- Tooth extractions caused by illness

❌ Usually Not Covered

- Dental cleanings

- Cosmetic dentistry

- Orthodontic procedures

- Pre-existing dental disease

Grooming and Hygiene Services

No standard pet insurance policy covers grooming. That means baths, haircuts, nail trims, ear cleaning, and similar services are fully out-of-pocket regardless of the plan.

This also extends to some services that feel medical but are classified as grooming: routine ear cleaning, anal gland expression when done as a standard preventive measure (as opposed to treating an infection), and routine nail trims.

Grooming isn’t covered. However, if a veterinarian diagnoses an illness that results from poor grooming—such as an ear infection—the medical treatment may qualify for coverage.

The exception comes when a grooming-adjacent issue becomes a genuine medical problem. If a dog develops an ear infection — not just needs routine ear cleaning — that treatment is a covered illness under Standard accident-and-illness policies. The trigger point is whether the service is preventive maintenance or treatment for a diagnosed condition.

Elective and Cosmetic Procedures

Pet insurance is built around medically necessary care. Anything elective — meaning it’s a choice, not a medical necessity — is excluded across virtually every standard policy.

Common elective exclusions include:

- Ear cropping — surgical alteration of ear shape, common in certain breeds

- Tail docking — removal of part of the tail

- Dewclaw removal — when done for cosmetic or convenience purposes rather than medical necessity

- Gastropexy — stomach tacking to prevent bloat, when performed as a preventive measure rather than emergency treatment

- Feline declawing

- Teeth whitening or cosmetic dental work

The line between elective and medically necessary can get complicated. Gastropexy performed during emergency bloat surgery would typically be covered. Gastropexy performed at the same time as a spay in a high-risk breed, as a preventive measure, is usually classified as elective and excluded.

If you’re considering a procedure that’s borderline — ask your insurer directly before scheduling. Get the answer in writing if possible.

If you’re considering a procedure that’s borderline — ask your insurer directly before scheduling. Get the answer in writing if possible.

Breeding and Pregnancy

Standard pet insurance policies don’t cover any costs related to breeding, pregnancy, whelping, or nursing. The reasoning insurers use is that pregnancy is a preventable condition — it can be avoided through spaying — so it doesn’t qualify as an unexpected illness or injury.

What this exclusion covers in practice:

- Prenatal veterinary care

- Pregnancy confirmation (ultrasound, X-ray)

- Whelping and labor complications

- Planned C-sections

- Nursing care and newborn health

- Artificial insemination and fertility treatments

- Progesterone testing

Some insurers offer breeding add-ons at an additional monthly cost — AKC Pet Insurance, Trupanion, and Rainwalk among them. These typically cover unexpected complications like emergency C-sections, pyometra, and mastitis, but not routine planned expenses. Dog breeding add-ons run approximately $39 to $158 per month depending on the insurer and your dog’s profile.

If your dog is pregnant at the time of enrollment, the pregnancy is classified as a pre-existing condition and excluded entirely.

Behavioral Conditions and Training

General pet behavior training is excluded from every standard policy. Obedience classes, behavioral training sessions, and the cost of professional trainers aren’t covered regardless of the situation.

The picture gets more nuanced with medically-diagnosed behavioral conditions. Some policies will cover diagnostics and treatment for behavioral disorders — anxiety, compulsive disorders, aggression with a medical basis — if they’re prescribed and managed by a licensed veterinarian. Others exclude behavioral treatment categorically.

If behavioral coverage matters to your situation — particularly for anxious dogs or those with diagnosed anxiety disorders — confirm the specific language with any insurer you’re considering. AKC Pet Insurance is among the providers that offer some behavioral coverage in certain states.

What’s universally excluded across all standard policies:

- Obedience training and general behavioral modification

- Dog training classes

- Board-and-train programs

- Behavioral medications purchased without a formal veterinary diagnosis and prescription

Behavioral medications purchased without a formal veterinary diagnosis and prescription.

Experimental and Investigational Treatments

If a treatment isn’t considered standard veterinary practice — clinical trials, investigational drugs, experimental therapies not accepted by the veterinary medical board in your state — it’s excluded.

This matters for owners dealing with cancer or rare conditions where conventional options have been exhausted and experimental treatments are being explored. Those costs fall entirely outside standard coverage.

Read more…Dog MRI Cost in the USA (2026): Average Cost, Insurance Coverage & Financing

Some alternative therapies that might seem experimental actually aren’t excluded. Acupuncture, chiropractic care, cold laser therapy, physical therapy, and hydrotherapy are covered under many accident-and-illness plans when prescribed by a licensed veterinarian to treat a covered condition. The determining factor is whether the therapy is treating a covered medical condition on a vet’s recommendation — not whether the treatment type sounds unconventional.

Herbal remedies, homeopathic treatments, and unproven supplements remain excluded.

Non-Veterinary Expenses

Insurance covers medical care. It doesn’t cover the costs that surround medical care. Excluded non-veterinary expenses include:

- Boarding and kennel fees (even during a hospitalization)

- Transportation and mileage to and from the vet

- Prescription food used for general nutrition management rather than active disease treatment

- Over-the-counter supplements and vitamins

- Waste disposal fees

- Record copying and access fees

- Administrative and bank fees

Prescription food is worth noting specifically. Many owners assume that if a vet prescribes a prescription diet, it’s covered. Many providers distinguish between prescription food used to actively treat a diagnosed medical condition versus food used to manage nutrition generally. The former may qualify in some policies; the latter typically does not.

Liability — If Your Dog Bites Someone

Pet insurance does not function as liability insurance. If your dog bites a neighbor, injures someone, or causes property damage, your standard pet insurance policy covers none of that.

Liability coverage for dog-related incidents typically lives under homeowners or renters insurance, which usually includes personal liability protection. That said, some breeds — Pit Bull Terriers, Rottweilers, German Shepherds, and others — may be excluded from liability coverage on certain homeowners policies depending on the insurer and state.

If you own a breed with any liability history or concerns, it’s worth reviewing your homeowners or renters policy separately. Some standalone dog liability policies also exist for this purpose.

Age Restrictions

Coverage varies won’t enroll puppies under 6–8 weeks of age, and older dogs face enrollment restrictions or limited coverage options past a certain age — typically around 14 years for many providers. Some providers, like MetLife, advertise that pets never “age out” of coverage once enrolled, but getting a senior dog newly enrolled into a policy comes with significant challenges.

Read more… 15 Organizations That Help Pay Vet Bills When You Can’t Afford Care (2026)

The practical takeaway: the window for enrolling a dog into comprehensive coverage is widest when they’re young and healthy. Every year that passes tends to mean more documented conditions, higher premiums, and narrower coverage options.

What’s Sometimes Covered — Just Not Always

A few exclusion areas vary significantly by insurer and plan. These are worth checking specifically before you choose a policy:

| Coverage Area | Some Plans Include It | Most Plans Don’t |

|---|---|---|

| Dental illness (not accident) | Embrace, ASPCA, Figo | Healthy Paws, some budget plans |

| Exam fees | Pets Best, ASPCA, others | Excluded on some plans |

| Alternative therapies (acupuncture, PT) | Most major plans | Excluded on accident-only plans |

| Behavioral treatment (diagnosed conditions) | AKC (select states), some others | Most standard plans |

| Prescription food (active disease treatment) | Some plans, limited | Most standard plans |

| Telehealth / virtual vet visits | Growing number of plans | Not universally included |

The Exclusion You’ll Most Regret Not Knowing About

Among everything on this list, dental disease and pre-existing condition exclusions cause the most financial pain — and the most surprised claims denials — because they’re both extremely common and extremely expensive.

Read more… Why Was My Pet Insurance Claim Denied? 5 Common Reasons (And How to Fix Them)

Dental disease affects the majority of dogs at some point in their lives. A dog that needed routine dental cleanings and didn’t get them can develop severe periodontal disease requiring extensive extractions and anesthesia — and if your policy doesn’t specifically include dental illness coverage, that bill is entirely yours.

Pre-existing conditions affect dogs at every life stage. The older a dog gets, the more their records accumulate — and every documented symptom is potential ammunition for a future denial.

Both are avoidable with the right policy selection from the start.

What to Do Before You Buy

Read the exclusions section of the sample policy — not the marketing page. Every major insurer makes sample policies available before purchase. The exclusions section, usually called “What We Do Not Cover,” tells you more than any comparison table ever will.

Read more…Emergency Vet Costs in the USA (2026): What You’ll Really Pay by State

Confirm dental illness coverage specifically. Ask directly: does this policy cover periodontal disease, extractions for dental illness, and dental infections? Or only accident-related dental injuries?

Get your dog’s vet records first. Know exactly what’s documented before you apply, so you can anticipate what might be flagged as pre-existing.

Call with a specific question about your dog’s health history. Insurers can explain how their policy would apply to a known condition, even if they won’t give a binding pre-authorization. The conversation will tell you something about how claims are handled.

Compare exclusion scope, not just premium. Two policies with nearly identical monthly costs can have meaningfully different exclusion lists. The cheaper policy may be excluding things that cost far more to pay out-of-pocket.

Comparison Table

| Coverage Area | Usually Excluded | Varies by Insurer |

|---|---|---|

| Dental illness | ❌ | ✅ |

| Exam fees | ❌ | ✅ |

| Behavioral therapy | ❌ | ✅ |

| Alternative therapies | ❌ | ✅ |

| Prescription food | ❌ | ✅ |

How to Read a Pet Insurance Policy Before Buying

Before you compare monthly premiums, take 10 minutes to read the insurer’s sample policy. Most pet insurance companies publish a sample policy online, and it tells you far more than any marketing page or comparison chart.

Start with the “What We Do Not Cover” section. This is where you’ll find the policy’s exclusions, including pre-existing conditions, waiting periods, dental limitations, routine care, and breed-specific restrictions. Understanding these exclusions before you enroll can help you avoid unexpected claim denials later.

Read more… Can’t Afford an Emergency Vet Bill? 15 Real Ways Dog Owners Find Help (2026)

Next, review the waiting periods for accidents, illnesses, and orthopedic conditions. Many policies require you to wait before coverage begins, and any condition that develops during that period is typically excluded. Waiting periods vary by insurer and coverage type.

Then check the reimbursement rate, deductible, and annual coverage limit. A lower monthly premium may come with a higher deductible, a lower reimbursement percentage, or a coverage limit that could leave you paying thousands of dollars out of pocket during a major emergency.

Read more… Emergency Vet vs Regular Vet Cost: Why Emergency Care Costs So Much More (2026)

Finally, understand the claims process. Find out how claims are submitted, what medical records may be required, how reimbursements are calculated, and how long payments usually take. Reading the full policy before you buy can prevent expensive surprises when you need coverage the most.

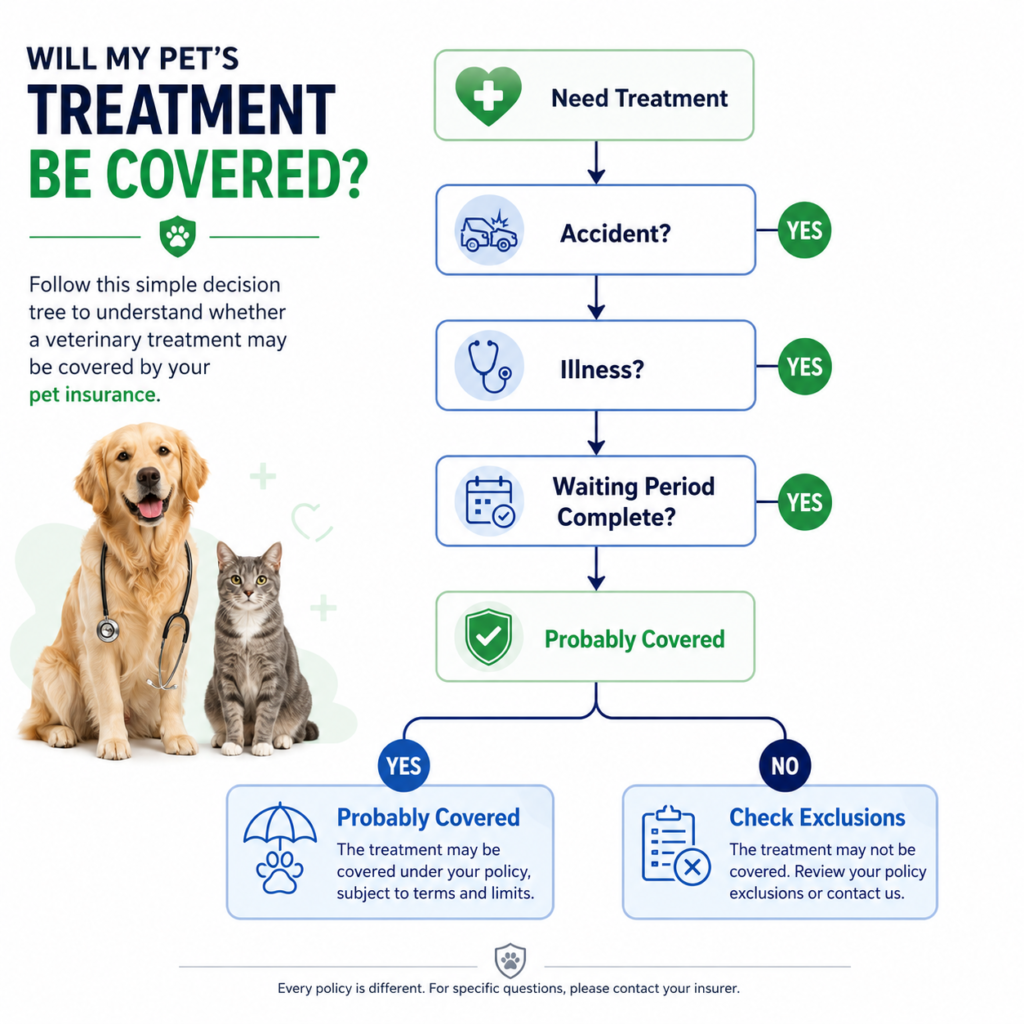

Decision Tree

Treatment Needed

↓

Unexpected illness?

↓

YES

↓

Policy active?

↓

YES

↓

Waiting period completed?

↓

YES

↓

Likely Covered

↓

NO

↓

Check Policy Exclusions

Read more… Best Vet Payment Plans in the USA (2026): CareCredit vs Scratchpay

Reviewed Sources & References

- NAPHIA (North American Pet Health Insurance Association)

- AVMA Pet Insurance Resources

- ASPCA Pet Health Insurance Coverage Overview

- AKC Pet Insurance Coverage FAQ

- Pets Best Coverage Details

- Healthy Paws Coverage & Exclusions

- Nationwide Pet Insurance Plan Restrictions

- Pumpkin Pet Insurance Exclusions Guide

- MetLife Pet Insurance Coverage & Exclusions

Final Thoughts

The best pet insurance policy isn’t always the cheapest one—it’s the one whose exclusions match your dog’s actual health risks. Before you compare premiums, compare what each insurer refuses to cover. Spending 10 minutes reading a sample policy today could save you thousands of dollars and prevent a denied claim when your dog needs treatment most.

Frequently Asked Questions

What does pet insurance usually not cover?

Most standard pet insurance policies exclude pre-existing conditions, routine wellness care, vaccinations, grooming, breeding expenses, cosmetic procedures, and liability claims. Some services, such as dental illness or alternative therapies, may be covered by certain insurers or optional add-ons, so always review the policy’s exclusions before enrolling.

Does pet insurance cover dental cleanings?

No. Routine dental cleanings are generally excluded from standard accident-and-illness plans. Some wellness add-ons reimburse preventive dental care. Coverage for dental disease, such as periodontal disease or tooth extractions, varies by insurer and policy. Always check whether your plan includes dental illness coverage before purchasing.

Does pet insurance cover spaying or neutering?

Standard accident-and-illness policies usually don’t cover spaying or neutering because they’re considered elective procedures. However, some wellness or preventive care plans may reimburse part of the cost as an optional benefit.

Does pet insurance cover flea, tick, and heartworm prevention?

No. Preventive medications such as flea, tick, and heartworm protection are generally excluded from standard policies. Many insurers offer wellness plans that provide a fixed annual reimbursement for these routine preventive treatments.

Does pet insurance cover breeding and pregnancy?

Most pet insurance plans exclude breeding, pregnancy, whelping, fertility treatments, and routine prenatal care. Some insurers offer optional breeding coverage that may help pay for unexpected complications, such as emergency C-sections or mastitis.

Will pet insurance pay if my dog bites someone?

No. Pet insurance only covers veterinary medical expenses for your pet. Injuries or property damage caused by your dog usually fall under homeowners or renters liability insurance rather than pet insurance.

Does pet insurance cover experimental treatments?

Usually not. Experimental drugs, clinical trials, and treatments that aren’t recognized as standard veterinary medicine are generally excluded. However, therapies such as acupuncture, rehabilitation, or physical therapy may be covered when prescribed by a veterinarian for a covered condition.

Does pet insurance cover prescription food?

Usually not. Most insurers exclude prescription diets used for general nutrition. Some plans may reimburse prescription food when it’s prescribed to treat a covered medical condition, but eligibility varies by insurer.

Can a pre-existing condition ever become covered?

Sometimes. Some insurers reconsider certain curable conditions after your pet has remained symptom-free for a specific period. Chronic or incurable conditions are generally excluded permanently. AKC Pet Insurance is one of the few major providers offering limited coverage for some pre-existing conditions after continuous coverage, subject to policy terms and state availability.

Why do pet insurance claims get denied?

The most common reasons include pre-existing conditions, waiting period exclusions, incomplete medical records, excluded treatments, policy limits, or claims submitted for services not covered under the policy. Reading the exclusions section before buying insurance can help reduce claim surprises.

Are all pet insurance exclusions the same?

No. Every insurer has different policy wording and optional coverage. One company may cover dental illness, exam fees, or alternative therapies, while another excludes them. Comparing exclusions—not just monthly premiums—is one of the smartest ways to choose a pet insurance policy.

Disclaimer: This article is for informational and educational purposes only. Cost data reflects 2026 national averages from NAPHIA, Insurify, and MetLife Pet Insurance and will vary based on your dog’s age, breed, location, and the specific plan you choose. PetInsurePrime does not sell pet insurance and receives no compensation from any insurance provider. Always compare multiple quotes and read your policy documents carefully before enrolling.

PetInsurePrime | Independent • Research-Based | Helping US dog owners understand real vet costs and coverage options — without the sales pressure.