Updated: June 2026 | Reading Time: 18 Minutes | Reviewed Sources: American Veterinary Medical Association (AVMA) CareCredit, Scratchpay, VetBilling

Quick Answer Vet Payment Plans

Yes, you can make monthly payments to a vet. Most veterinary clinics do not offer direct payment plans themselves, but many work with financing providers such as CareCredit and Scratchpay that allow pet owners to spread veterinary costs into monthly installments. Some independent clinics also offer in-house payment plans for established clients.

In this guide, you’ll learn how vet payment plans work, which financing options are available, their pros and cons, and what to do if you can’t afford a veterinary bill upfront.

Quick Comparison of Vet Payment Plan Options

| Payment Option | Credit Check | Monthly Payments | Best For |

|---|

| CareCredit | Yes | Yes | Good credit |

| Scratchpay | Soft inquiry | Yes | Lower credit |

| VetBilling | Usually No | Yes | Existing clients |

| Wellness Plan | No | Yes | Preventive care |

The Three Types of Vet Payment Plans

Understanding the structure before you apply makes the process significantly less stressful.

Type 1: Third-Party Financing (Most Common)

A financing company pays the vet in full. You repay the financing company in monthly installments — with or without interest, depending on the plan you qualify for.

The two dominant players: CareCredit and Scratchpay. Both are widely accepted at veterinary clinics across the US. Both offer near-instant approval decisions. Both can be applied for on a smartphone in the waiting room.

This is what most people mean when they say “the vet offers payment plans.” The vet itself isn’t the lender.

Type 2: In-House Payment Plans (Less Common, More Flexible)

Some clinics — especially independent practices and those using platforms like VetBilling — offer direct payment arrangements. You pay the clinic in installments, bypassing any external lender.

In-house veterinary payment plans are financing options offered directly through your veterinary hospital. Instead of paying the entire bill at the time of your pet’s care, some hospitals allow a billing and statement system that you pay in monthly installments. However, veterinarians aren’t bankers or lenders, and setting up these payment plans can put their businesses at risk, so you may struggle to find a vet who offers them.

The advantage: no credit check required in many cases, and the terms can be more flexible. The disadvantage: harder to find, typically reserved for established clients, and availability is entirely at the clinic’s discretion.

Type 3: Wellness Plans (Preventive Care, Not Emergency)

Wellness plans are monthly membership programs — typically $30–$80/month — that spread the cost of routine, preventive care across the year. Annual exams, vaccines, heartworm prevention, and dental cleanings are bundled into a flat monthly payment.

Wellness plans are not emergency financing. They don’t help when your dog needs surgery tonight. They exist to make routine care more financially predictable over time.

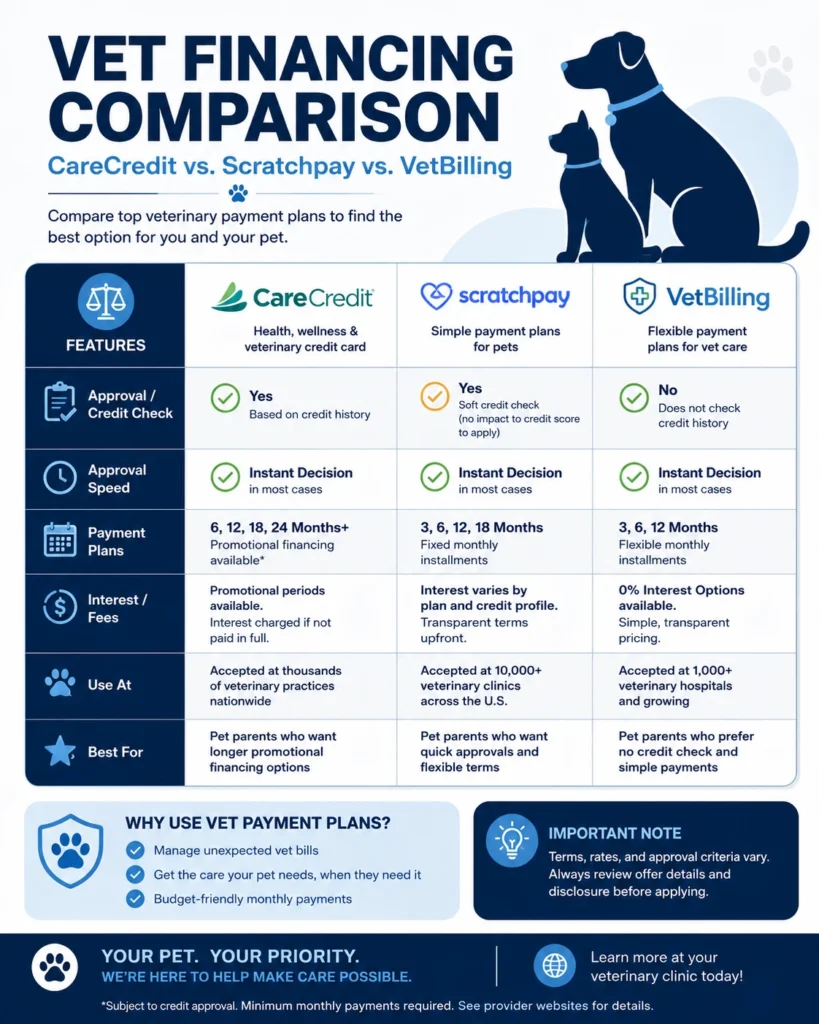

CareCredit vs Scratchpay vs VetBilling — The Real Comparison

These three options cover the vast majority of vet financing situations in the US. Here’s how they actually work — including the details most people don’t find out until after they’ve applied.

| Feature | CareCredit | Scratchpay | VetBilling |

|---|---|---|---|

| Type | Revolving credit card | Fixed installment loan | In-house installment plan |

| Network size | 275,000+ providers (~75% of US vets) | ~17,000 vet clinics | Partner clinics only |

| Credit check | Hard inquiry (affects credit score) | Soft inquiry (does not affect score) | No credit check |

| 0% APR offer | Yes — 6, 12, 18, or 24 months | Yes — on qualifying plans | Yes — set by clinic |

| Interest if not paid off in time | Retroactive 26.99% APR from day one | Retroactive interest on some plans | Varies by clinic |

| Best for | Reusable credit, multiple pets, good credit | One-time bill, lower credit score | Credit-constrained clients with established vet relationship |

| Reusable after payoff | Yes | No — new application per procedure | Varies |

| Apply at | carecredit.com | scratchpay.com | Through participating vet clinic |

CareCredit — The Biggest Network, The Biggest Warning

CareCredit is accepted at over 275,000 healthcare providers — about 75% of US vet clinics. This network size is its biggest advantage. For most people, their vet already accepts it.

The deferred interest warning — read this before applying:

CareCredit offers longer promotional 0% APR periods up to 24 months, but be warned: these are retroactive interest charge promotions. If you don’t pay the full balance before the promo ends, interest charges at 26.99% APR are applied retroactively to the original purchase date.

This is one of the most important terms to understand before accepting a promotional financing offer.

CareCredit requires a formal credit card application with a hard inquiry. Approval typically requires a fair to good credit score. If denied, the hard inquiry still appears on your credit report, which could temporarily lower your score without any benefit.

Who CareCredit is right for: Good-to-excellent credit, reusable financing for multiple pets or ongoing care, ability to pay off the balance before the promotional period ends.

Read more…Dog Spinal Surgery Cost in the USA: What Most Owners Pay in 2026

Scratchpay — Better for Lower Credit, Cleaner Terms

Scratchpay is not a credit card. It’s a single-purpose installment loan tied to one specific vet bill. You apply, get approved for that amount, make fixed monthly payments, and the loan closes when it’s paid off.

Scratchpay offers 12–24 month plans for amounts between $200–$10,000, with no hidden fees.

Scratchpay may be more appropriate in these situations: you want to explore financing options without impacting your credit score, you prefer fixed predictable monthly payments with a clear end date, you want to avoid the risk of deferred interest charges, or your credit profile makes traditional credit card approval uncertain.

The tradeoff: Scratchpay covers roughly 17,000 locations — significantly smaller than CareCredit’s network. Confirm your clinic accepts it before applying.

APR on Scratchpay ranges from 0% (for qualified applicants on short-term plans) up to 36% for longer-term plans with lower credit scores. The key difference from CareCredit: the rate you’re approved for is fixed and transparent upfront. No retroactive interest surprises.

Who Scratchpay is right for: Lower or limited credit history, preference for fixed monthly payments, one-time bill rather than ongoing care costs, avoiding hard credit inquiry risk.

Read more…Dog Surgery Cost in the USA: Real Prices for 2026

VetBilling — When Both Others Say No

VetBilling is a platform that allows veterinary clinics to offer in-house payment plans without the administrative burden of managing them internally. If your vet uses VetBilling, you can set up a direct installment arrangement — no external credit check, no bank involved.

VetBilling allows veterinarians to offer in-house payment plans, prepayment and wellness plan billing to pet owners at no cost to their practice.

The approval is based on your relationship with the clinic, not your credit score. An established client who’s been coming for three years with a good history has a much better chance than a first-time visitor.

VetBilling isn’t available at every clinic — ask directly whether your vet uses it or offers any equivalent in-house arrangement.

Who VetBilling is right for: Clients denied by both CareCredit and Scratchpay, established clients at partner clinics, situations where clinic relationship matters more than credit score.

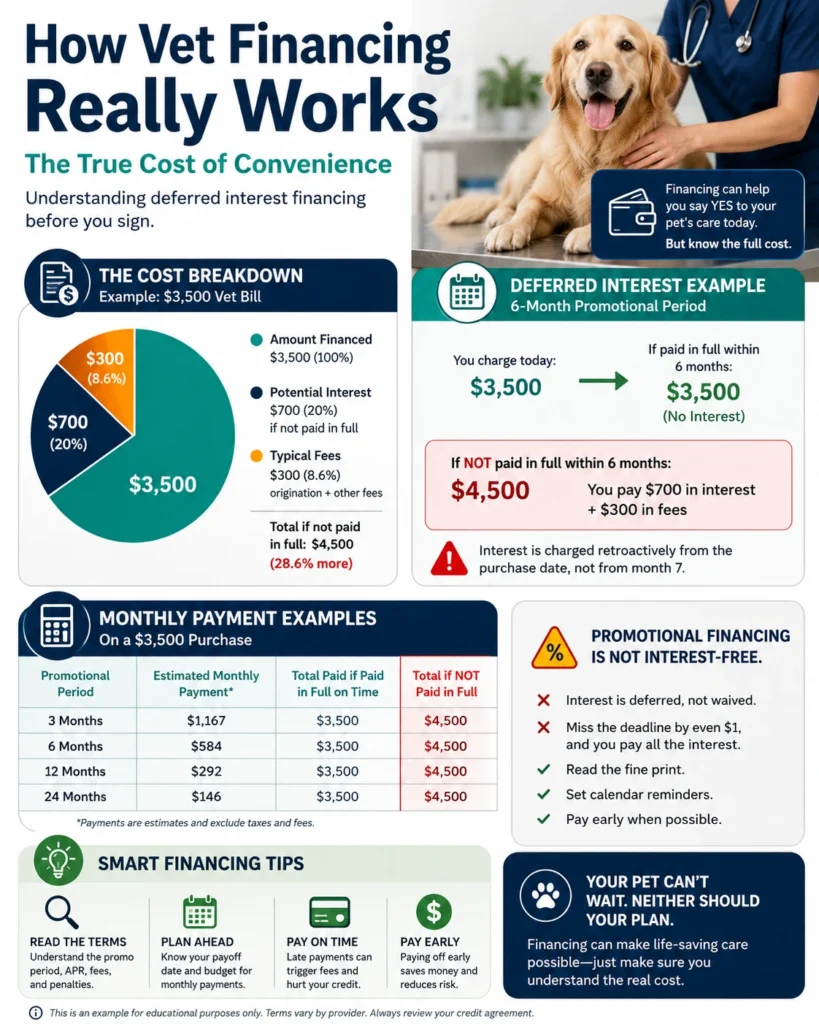

The Deferred Interest Problem — What Most People Learn Too Late

Both CareCredit and some Scratchpay plans offer “0% interest for X months” promotions. These sound straightforward. They’re not — and the fine print is where the financial damage happens.

Some promotional financing offers may include deferred-interest terms. Always review the specific terms of your plan before accepting financing.

What that means in practice:

Example: You finance a $3,500 vet bill on a 12-month 0% promotional plan. Your monthly payment to clear it in 12 months is about $292. You pay on time for 11 months and have $300 left. In month 12, something unexpected happens and you can only pay $100.

You don’t owe interest on the remaining $200. You owe 26.99% APR on the entire original $3,500, calculated from the date you first made the charge. That could add $800–$900 to what you owe.

How to protect yourself:

- Calculate the exact monthly payment needed to zero out the balance by the last day of the promotional period — not the minimum payment

- Set a calendar reminder 30 days before the promo period ends

- If you’re not confident you can pay it off in time, choose a fixed-rate installment plan instead of the 0% promo option — the interest rate will be higher, but it’s predictable

Always calculate the monthly payment needed to hit zero before the deadline.

In-House Vet Payment Plans — What They Are and How to Ask

The most flexible payment arrangement is also the hardest to find: a direct deal with your veterinarian, no outside lender involved.

Some hospitals provide no-interest payment plans, depending on the bill amount and how long you’ve been a client. Many veterinary hospitals use third-party rather than in-house payment plans.

When in-house plans exist, they typically look like this:

- A partial payment upfront (usually 20–50% of the total)

- Remaining balance divided into 2–6 monthly installments

- No formal credit application — based entirely on the clinic’s trust in you

- Sometimes interest-free; sometimes with a small administrative fee

These plans are significantly more likely to be available if:

- You’ve been a client at this practice for at least 1–2 years

- You have a history of paying your bills on time

- The bill is for a known, documented emergency (not a pattern of delayed payments)

- You’re honest and upfront about your situation before the visit, not after

For many clients who are credit-constrained, in-house plans mean they can still obtain a plan even if a bank or third-party lender has declined their application.

What to Say — Exact Phrases That Open the Conversation

Most payment plan options don’t get offered unless you ask. The framing matters.

What works:

“I want to take care of this bill. I don’t have the full amount today — do you offer any payment arrangements, or do you work with CareCredit or Scratchpay?”

This signals good faith and names specific options. Clinics that accept third-party financing will direct you to apply on the spot. Clinics that offer in-house plans will often open that conversation once they know you’re asking.

“I’m an established client here and I’ve always paid on time. Is there any flexibility on how I can pay this balance over the next few weeks?”

For long-term clients, this framing works. It invokes the relationship directly.

“Can I apply for Scratchpay right now while you finish the discharge paperwork?”

Naming Scratchpay specifically is useful — it tells the front desk you know what you’re asking for and you’re ready to act immediately.

What doesn’t work:

Saying nothing and hoping the bill can be sorted out later. Most clinics expect payment at discharge. A plan that isn’t established before you leave is significantly harder to negotiate afterward.

Vague promises — “I’ll pay you back, I just need time” — without proposing any specific structure. A concrete plan (partial payment now + specific installments) is dramatically more persuasive than an open-ended request.

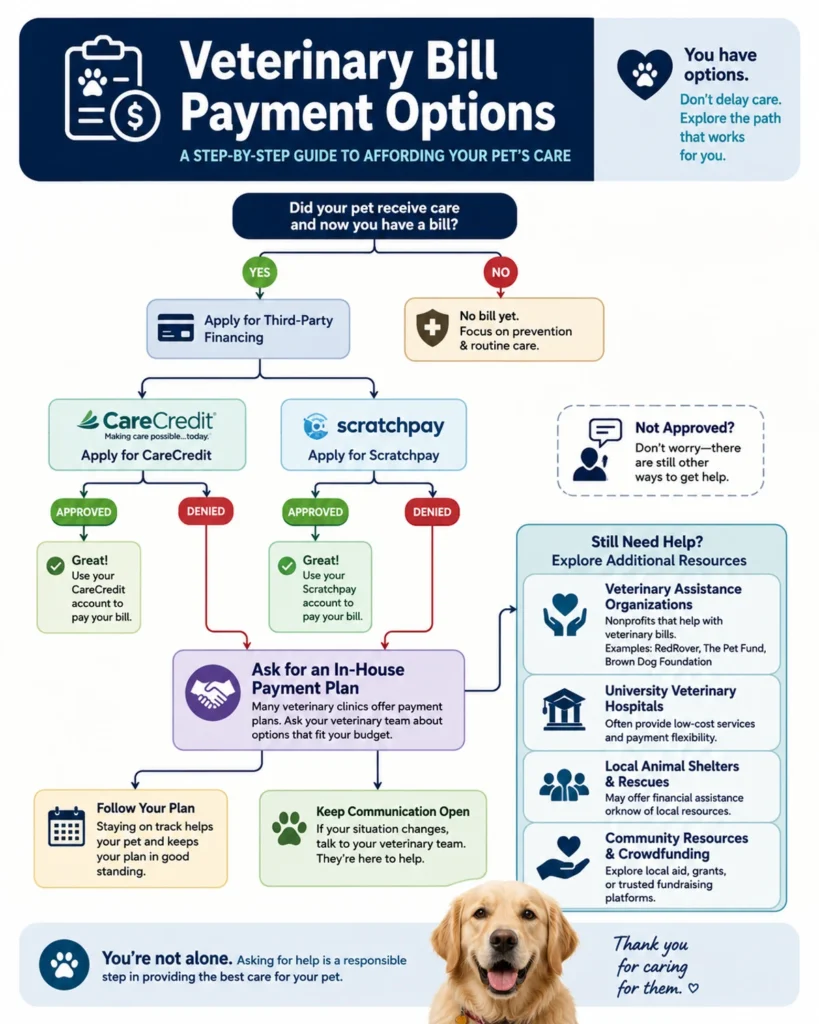

What If You’re Denied for Both CareCredit and Scratchpay?

The 40% approval rate on third-party financing means that if your practice offers only one option, the majority of clients who need help do not get it.

Being denied doesn’t close every door. In order:

1. Ask about VetBilling or in-house plans. If the clinic uses VetBilling or has its own arrangement, credit score isn’t the determining factor — the relationship is. This is especially true at independent practices.

2. Be direct about your situation. “I was just denied for CareCredit. Is there anything your clinic can do directly?” This conversation, held honestly at the front desk, sometimes surfaces options that weren’t volunteered.

3. Explore nonprofit grants in parallel. RedRover Relief, Frankie’s Friends, and Bow Wow Buddies Foundation can be applied for on the same day. These don’t require credit approval — only financial documentation.

4. University veterinary hospitals. If the procedure allows any flexibility in timing, AVMA-accredited teaching hospitals perform the same procedures at 30–60% lower cost, which may bring the total into a range that’s manageable without financing at all.

[→ Read: 15 Organizations That Help Pay Vet Bills When You Can’t Afford Care

What If You Can’t Afford a Vet Bill Today?

Many pet owners searching for vet payment plans aren’t simply comparing financing options — they’re trying to figure out how to get their pet treated when they don’t have enough money available right now.

Read more…Can’t Pay a Vet Bill in the USA? Here’s What Actually Happens (2026)

If you can’t afford a vet bill upfront, consider:

- Asking about in-house payment plans

- Applying for nonprofit veterinary assistance programs

- Exploring family or emergency funding options

- Contacting local animal welfare organizations

- Seeking treatment at university veterinary hospitals when appropriate

The earlier you discuss payment concerns with the clinic, the more options you’re likely to have.

Read more… Dog Spinal Surgery Cost in the USA

Does Getting a Vet Payment Plan Affect Your Credit Score?

It depends on which type you use.

| Option | Credit Impact |

|---|---|

| CareCredit application | Hard inquiry — temporary score drop of 5–10 points |

| CareCredit if denied | Hard inquiry still appears even if denied |

| Scratchpay eligibility check | Soft inquiry — no score impact |

| VetBilling / in-house plan | No credit check — no impact |

| Credee | No credit check — no impact |

| Personal loan (bank/credit union) | Hard inquiry on application |

| Missing payments on any plan | Negative mark if sent to collections |

CareCredit requires a formal credit card application with a hard inquiry. If denied, the hard inquiry still appears on your credit report, which could temporarily lower your score without any benefit. This is worth knowing before applying — if your credit is uncertain, trying Scratchpay first makes more sense since its eligibility check is a soft pull.

How to Use a Vet Payment Plan Responsibly

Getting approved is the beginning, not the end. A few practical notes:

Calculate your actual monthly payment before accepting. Don’t just accept whatever minimum the plan suggests. Calculate what you need to pay monthly to clear the balance before any promotional period ends.

Don’t stack two promotional plans on the same bill. Applying for both CareCredit and a personal loan to cover one bill creates two separate obligations. If you can’t keep up with both, the consequences compound.

Treat it like any other debt. Missed payments on CareCredit and Scratchpay can be sent to collections. This affects your credit score and makes the next emergency harder to finance.

Wellness plans are separate. If your clinic offers a monthly wellness plan, enrolling in it for future routine care is a smart complement to emergency financing — not a replacement for it.

Vet Payment Plans vs Pet Insurance

Vet payment plans help you manage costs after a bill arrives.

Pet insurance helps reduce the financial impact of covered treatments before the emergency happens.

Financing and insurance solve different problems, but many pet owners use both together to manage unexpected veterinary expenses.

Read more…Pet Insurance for Dogs in the USA: How It Works (2026)

Key Takeaway

Most pet owners can make monthly payments to a vet through third-party financing providers such as CareCredit or Scratchpay. Some independent veterinary clinics also offer in-house payment plans for established clients. The best option depends on your credit profile, your veterinarian’s policies, and how quickly you can repay the balance without triggering additional interest charges.

If you’re facing a large veterinary bill, it’s also worth understanding the total cost of common procedures before choosing a financing option. Read more….Dog Surgery Cost in the USA Read more…Emergency Vet Visit Cost at Night in the USA

Important Note

Financing terms, approval requirements, interest rates, and provider participation may change over time. Always review the lender’s current terms and speak directly with your veterinary clinic before making a financing decision.

This article is for educational purposes only and should not be considered financial advice.

Actionable Summary

If you’re at the vet right now with a bill you can’t pay in full:

- Ask immediately: “Do you accept CareCredit or Scratchpay?”

- Apply for Scratchpay first if your credit is uncertain — soft inquiry, no score impact

- Apply for CareCredit if your credit is solid and the clinic accepts it

- Ask about VetBilling or in-house plans if both are declined

- Apply to RedRover Relief the same day for emergency grant assistance

Before your next vet visit (preparation):

- Check scratchpay.com to see if your clinic is listed

- Check carecredit.com/find-care to confirm your clinic accepts it

- Consider pre-checking your Scratchpay eligibility — it’s a soft pull and takes two minutes

If you’re denied everywhere:

- Try Credee (no credit check required)

- Have a direct conversation with the clinic about in-house options

- Apply to nonprofit grants (RedRover, Frankie’s Friends, Bow Wow Buddies)

- Contact the nearest university veterinary hospital — same care, 30–60% lower cost

Frequently Asked Questions

Can you really make monthly payments to a vet?

Yes. Most veterinary clinics work with financing providers such as CareCredit or Scratchpay that allow pet owners to spread treatment costs into monthly payments. Some independent clinics also offer in-house payment plans for established clients.

What is the difference between CareCredit and Scratchpay?

CareCredit is a reusable healthcare credit card, while Scratchpay is a fixed installment loan for a specific veterinary bill. CareCredit has a larger provider network, while Scratchpay may be easier to qualify for and uses a soft credit check.

What is deferred interest on a vet payment plan?

Deferred interest means you may owe interest on the entire original balance if the promotional period ends before the debt is fully repaid. Always review the financing terms carefully before accepting a payment plan.

What if I have bad credit — can I still get a vet payment plan?

Possibly. Some financing providers have more flexible approval requirements, and certain veterinary clinics offer in-house payment arrangements for established clients. It’s worth asking your vet about all available options.

How do I ask my vet for a payment plan?

Ask before treatment is completed whenever possible. A simple approach is: “Do you offer payment plans, or do you work with financing providers such as CareCredit or Scratchpay?”

Does applying for a vet payment plan hurt my credit?

It depends on the provider. Some financing options require a hard credit inquiry, while others use a soft inquiry or no credit check at all. Review the application terms before applying.

Can I use a vet payment plan for a routine visit?

Yes. Many payment plans can be used for routine care, dental procedures, vaccinations, diagnostics, and emergency treatment, depending on the provider and clinic.

Do all veterinarians offer payment plans?

No. Some clinics offer financing directly or through third-party providers, while others require payment in full at the time of service. Always ask your veterinary clinic about available payment options.

Can I get emergency veterinary care if I can’t pay the full bill today?

Possibly. Many clinics work with financing providers, and some offer in-house arrangements for established clients. Discuss payment concerns with the clinic as early as possible to explore available options.

Disclaimer

This article is for informational and educational purposes only. Financing terms, APR ranges, network sizes, and approval requirements for CareCredit, Scratchpay, VetBilling, and Credee are based on publicly available information as of 2026 and are subject to change. PetInsurePrime does not sell pet insurance or financial products and receives no compensation from any financing company listed. Always review the full terms and conditions of any financing agreement before signing. PetInsurePrime does not provide financial advice — consult a licensed financial advisor for guidance specific to your situation.

PetInsurePrime | Independent • Research-Based | Helping US dog owners understand real vet costs and coverage options — without the sales pressure.