Updated: June 2026 | Reading Time: 18 Minutes | Reviewed Sources: NAIC, Money, Bankrate, ManyPets

Key Takeaways

✓ Pre-existing conditions are the most common reason claims are denied.

✓ Documentation issues are often the easiest to fix.

✓ Many denied claims can be appealed with additional medical records.

✓ Some U.S. states now provide stronger consumer protections for pet insurance claims.

Quick Answer Why Was My Pet Insurance Claim Denied?

Most pet insurance claims are denied because of:

- Pre-existing conditions

- Waiting periods

- Policy exclusions

- Missing documentation

- Coverage limits

A denial doesn’t always mean your claim is over. Many insurers allow appeals, especially when additional veterinary records or documentation are available.

Read more… Pet Insurance for Dogs in the USA: How It Works (2026)

In This Guide

Why Claims Get Denied

Most Common Reasons

How to Appeal

State Laws

Avoid Future Denials

Financial Help

Step One: Read the Denial Letter Carefully

Before anything else, the denial letter itself is the most important document you have. The denial notice should clearly explain why your claim was rejected, and outline the process for appealing the decision.

Look specifically for:

- The exact reason code or category cited (pre-existing condition, exclusion, waiting period, documentation, coverage limit)

- Whether the denial references a specific date, prior vet visit, or medical record

- Whether an appeal process and deadline are mentioned

- Contact information for questions or additional documentation requests

Important

Never throw away your denial letter.

You’ll usually need it when filing an appeal or contacting your state’s insurance regulator.

Sometimes the fix is a simple paperwork error, like a missing page from your vet’s invoice. If you’re still unclear why the claim was denied, call your pet insurance company directly. Ask what additional details and documentation are needed and if there’s a deadline for filing an appeal. Take notes — including the date, time, and the name of the representative you spoke with.

The Most Common Reasons Pet Insurance Claims Get Denied

1. Pre-Existing Conditions (The #1 Reason)

Pre-existing conditions are the leading reason pet insurance claims get denied. However, many pet owners misunderstand what insurers actually consider “pre-existing.” Before assuming your claim was denied correctly, it’s important to understand how these decisions are made.

What Is a Pre-Existing Condition?

A pre-existing condition is any illness, injury, or symptom your pet had before your policy became eligible for coverage. Importantly, a formal diagnosis isn’t always required. In many cases, insurers review past veterinary records for clinical signs that may indicate the condition existed before coverage started.

Why Do Insurers Deny These Claims?

Imagine your dog had a mild limp noted during a routine check-up two years before you purchased insurance. Later, your dog tears an ACL and requires surgery. The insurer may argue the earlier limp was an early sign of the same condition and classify the injury as pre-existing.

This is why reviewing your pet’s complete medical history is one of the first steps insurers take during claims processing.

What Are Bilateral Exclusions?

Some insurers apply what’s known as a bilateral exclusion for certain orthopedic conditions. Because bilateral exclusions vary by insurer, always read your policy wording carefully before assuming a second injury will be covered.

Check your state’s Department of Insurance website to see which consumer protections apply where you live.

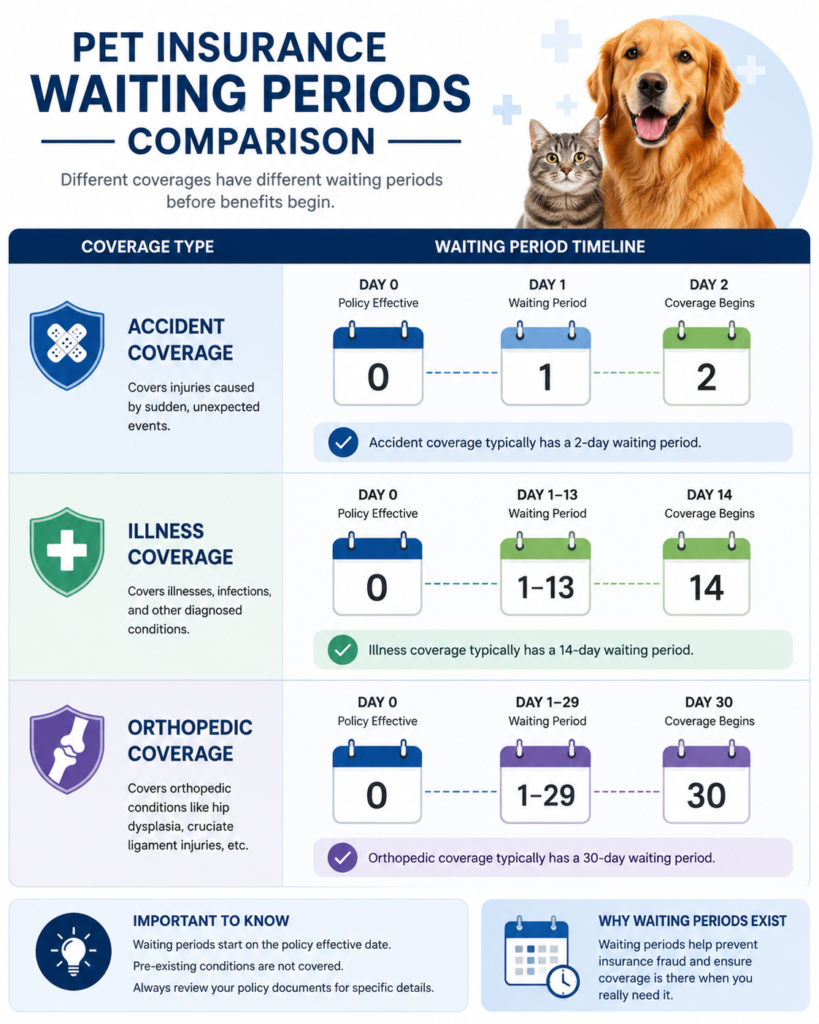

2. Waiting Periods

| Coverage Type | Typical Waiting Period | Common Examples | Can It Be Waived? |

|---|---|---|---|

| Accidents | 0–5 days (varies by insurer and state) | Broken bones, swallowed objects, cuts | Rarely |

| Illnesses | Around 14 days (some plans use 30 days) | Ear infections, vomiting, pneumonia | No |

| Orthopedic Conditions | 30 days to 6 months (or longer with some insurers) | ACL tears, hip dysplasia, luxating patella | Sometimes, after a qualifying veterinary exam or depending on the insurer |

| Policy Renewal | Usually no new waiting period (where applicable) | Existing policy renewal | Yes – renewals generally don’t restart the original waiting period under many policies and newer regulatory frameworks |

3. Policy Exclusions (Not Covered Under Your Plan)

Not every denied claim is caused by a pre-existing condition or waiting period. Sometimes, the treatment simply isn’t included in your policy.

While exclusions vary by insurer, they generally fall into two categories: common exclusions found in most plans and policy-specific exclusions that depend on your provider and coverage.

Most Common Exclusions

These are the exclusions pet owners encounter most often:

- Routine and preventive care – Annual wellness exams, vaccinations, flea/tick prevention, routine dental cleanings, and spay/neuter procedures are usually not covered unless you’ve purchased a wellness add-on.

- Pre-existing conditions – Any illness, injury, or symptoms that existed before your policy became effective are typically excluded.

- Waiting period claims – Treatments received before the waiting period ends aren’t eligible for reimbursement, even if your policy is active.

- Cosmetic or elective procedures – Ear cropping, tail docking, declawing, and other non-medically necessary procedures are generally excluded.

Less Common or Policy-Specific Exclusions

These exclusions don’t apply to every policy but are important to review before assuming you’re covered:

- Behavioral therapy or training – Treatment for anxiety, aggression, or behavioral modification may require an optional rider or may not be covered at all.

- Breeding and pregnancy expenses – Pregnancy, breeding, whelping, fertility treatments, and newborn care are commonly excluded.

- Commercial or working animals – Dogs used for breeding, racing, security, hunting, or commercial activities may need specialized insurance instead of a standard pet policy.

- Age, breed, hereditary, or congenital restrictions – Some insurers place limitations on certain hereditary conditions, breed-related illnesses, or coverage for older pets, while others provide broader protection depending on the policy terms.

Tip: Never assume all pet insurance policies have the same exclusions. Always read your policy’s “Exclusions” section before filing an appeal. Sometimes a claim is denied simply because the treatment isn’t included—that feel arbitrary even when they’re technically within the policy’s terms. Read the fine print and understand policy exclusions thoroughly before purchasing — but if you’re past that point and holding a denial, the next section covers what to do.

4. Documentation Issues

Documentation Checklist

✓ Itemized Invoice

✓ Medical Records

✓ Vet Notes

✓ Claim Form

✓ Signature

✓ Policy Number

5. Coverage Limits Reached

Most pet insurance policies include reimbursement limits, such as an annual limit, a per-condition limit, or (less commonly) a lifetime limit. Once you reach that limit, your insurer won’t reimburse any additional covered expenses until the next policy period begins—or at all, depending on your plan.

Example:

Imagine your policy has a $10,000 annual reimbursement limit.

- January: Your dog undergoes emergency surgery — $4,500 reimbursed

- April: Cancer treatment — $3,000 reimbursed

- September: Hospitalization — $2,500 reimbursed

At this point, you’ve reached your $10,000 annual limit.

Now, if your dog needs another covered procedure in November costing $2,000, your insurer may deny reimbursement for that claim—not because the treatment isn’t covered, but because your annual reimbursement limit has already been exhausted. Coverage typically resets when your new policy year begins.

What you should do:

- Check whether your policy has an annual, per-condition, or lifetime reimbursement limit.

- Review your insurer’s explanation of benefits (EOB) to see how much coverage you’ve already used this policy year.

- If your pet has an ongoing medical condition, consider choosing a higher or unlimited annual reimbursement limit when your policy renews, if your insurer offers that option.

💡 Tip: A claim denied because you’ve reached your coverage limit is different from a claim denied due to a pre-existing condition or policy exclusion. In this case, the treatment may still be covered under your policy—you’ve simply reached the maximum reimbursement available for the current policy year.

Quick Reference: Denial Reason → What It Means → Can You Appeal?

| Denial Reason | What It Means | Appeal Likelihood |

|---|---|---|

| Pre-existing condition (with clear prior diagnosis) | Documented diagnosis exists before policy start | Low — but worth checking if conditions are medically distinct |

| Pre-existing condition (vague/no diagnosis) | Insurer inferred connection from a minor note | Moderate to high, especially in regulated states |

| Bilateral exclusion | Same condition, opposite side of body | Moderate — vet letter explaining distinct injury can help |

| Waiting period | Incident occurred before coverage activated | Low — but check your state’s waiting period caps |

| Policy exclusion (clear, named) | Condition/treatment explicitly not covered | Low |

| Policy exclusion (vague language) | Ambiguous wording used to deny | Moderate to high |

| Documentation issue | Missing records, incomplete forms, late submission | High — usually resolvable |

| Coverage limit reached | Annual/lifetime cap already hit | Low |

How to Appeal a Denied Pet Insurance Claim (Step-by-Step)

If you believe your claim was denied incorrectly, follow this process before giving up.

Step 1: Read Your Denial Letter Carefully

Before collecting documents or contacting your veterinarian, carefully read your denial letter. It explains exactly why your claim was rejected and tells you whether you have the right to appeal.

Pay attention to:

- The denial reason

- Policy section referenced

- Appeal deadline

- Missing documentation

- Contact details for the claims department

Step 2: Collect Every Supporting Document

Required Documents

✓ Denial Letter

✓ Itemized Vet Invoice

✓ Medical Records

✓ Diagnostic Reports

✓ X-rays

✓ Blood Test Results

✓ Claim Form

✓ Policy Number

Step 3: Ask Your Veterinarian for a Medical Support Letter

Your veterinarian’s opinion often becomes the strongest piece of evidence during an appeal.

If your claim was denied because of a pre-existing condition, ask your veterinarian to explain whether the current diagnosis is medically different from any previous symptoms or conditions.

Pro Tip : A detailed letter from your veterinarian can strengthen appeals involving pre-existing condition disputes, especially when it clearly explains why the current condition is unrelated to earlier symptoms.

Step 4: Submit Your Appeal Before the Deadline

Before Clicking Submit

✓ Appeal Form

✓ Vet Letter

✓ Medical Records

✓ Invoices

✓ Diagnostic Reports

✓ Written Explanation

Step 5: Keep Records of Every Conversation

Save copies of every email, upload confirmation and appeal document.

Whenever you speak with your insurance company, write down:

Date

Representative Name

Reference Number

Summary of Conversation

These notes become valuable if your appeal needs further review.

Step 6: Escalate Your Case to Your State Department of Insurance

Before filing a complaint, make sure you’ve completed your insurer’s internal appeals process.

When filing a complaint, include:

- Original denial letter

- Appeal documents

- Medical records

- Communication history

- Policy information

State insurance departments investigate whether insurers followed applicable laws and policy requirements when handling claims.

Quick Summary

Appeal Checklist

✓ Read the denial letter

✓ Collect all medical records

✓ Request a vet support letter

✓ Submit a complete appeal

✓ Keep communication records

✓ Contact your state regulator if necessary

Read more… Vet Payment Plans: Can You Make Monthly Payments to a Vet? (2026)

What Your State’s Regulations Mean for Your Claim

A growing number of U.S. states have adopted pet insurance regulations based on the National Association of Insurance Commissioners (NAIC) Pet Insurance Model Act. These laws are designed to improve transparency and strengthen consumer protections by requiring clearer policy disclosures, standardized definitions, and fairer claims-handling practices.

Because adoption varies by state and continues to evolve, the protections available to pet owners may differ depending on where they live. Before assuming a denied claim is final, check your state’s Department of Insurance to understand the rules that apply in your state.

How These Regulations May Help Pet Owners

In states that have adopted pet insurance regulations based on the NAIC Model Act, policyholders may benefit from protections such as:

- Clearer disclosure of policy exclusions and waiting periods before purchase.

- Standardized definitions for important terms like “pre-existing condition.”

- More transparent claims-handling procedures.

- Better consumer protections when disputes arise between insurers and policyholders.

The exact protections depend on your state’s laws, so always review your policy and your state’s insurance regulations before filing an appeal.

Real Example: How Regulation Changes the Outcome

A useful illustration of how much this matters:

Scenario — “Luna,” 3-year-old mixed breed in a regulated state. Luna is diagnosed with hip dysplasia. A vet chart from two years earlier noted “minor stiffness” — but no diagnosis was ever made.

Without regulation: Claim denied. The “stiffness” note is used to classify the dysplasia as pre-existing. Owner pays $4,500 out of pocket.

With 2026 regulation: Claim approved. The insurer cannot prove the stiffness was definitively hip dysplasia — there’s no clear medical evidence connecting the two. After a $250 deductible and 90% reimbursement, insurance pays $3,825.

Same dog, same medical history, same claim — different outcome based entirely on which state’s regulatory framework applies. This is precisely why checking your state’s status before assuming a pre-existing denial is final matters.

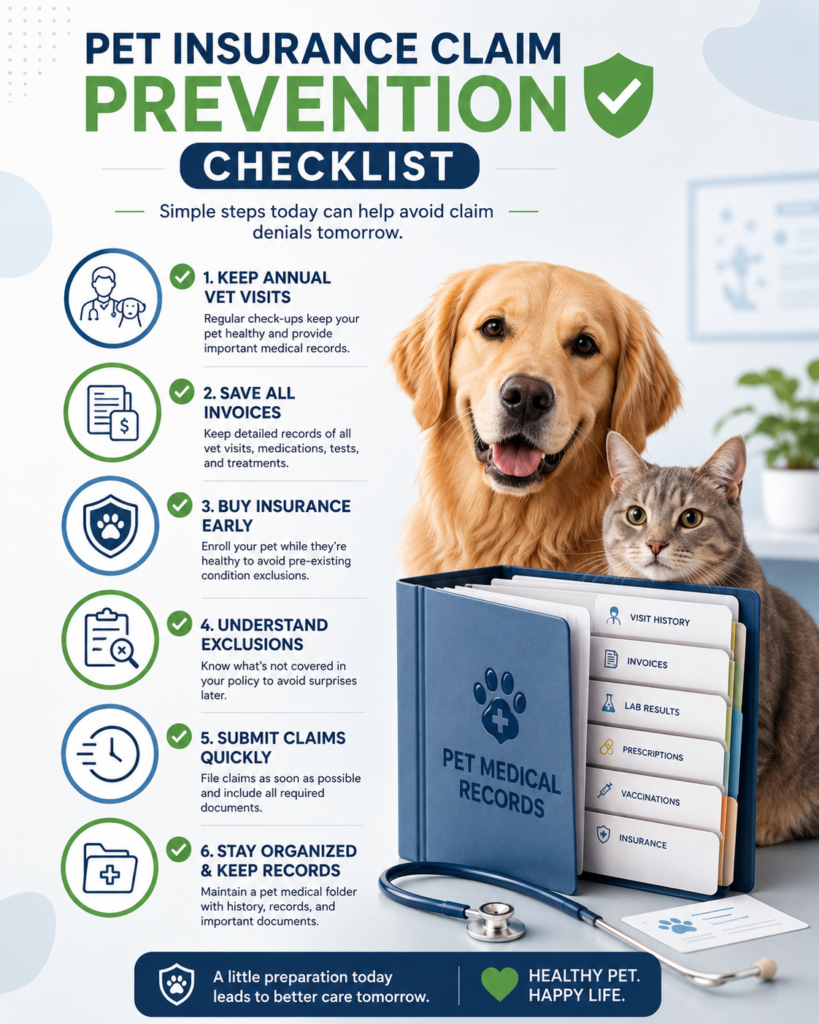

How to Avoid Future Denials

Once your current situation is resolved, a few practices reduce denial risk going forward:

Future Claim Checklist

✓ Buy insurance early

✓ Keep annual vet records

✓ Read exclusions

✓ Submit claims quickly

✓ Save all invoices

What If You Can’t Afford to Wait for an Appeal?

Appeals take weeks, sometimes longer — and the vet bill is due now regardless of the outcome. If you’re facing this gap:

Read more… Best Vet Payment Plans in the USA: CareCredit vs Scratchpay

CareCredit or Scratchpay can bridge the timing gap — pay the bill now through financing, and if your appeal succeeds, use the insurance reimbursement to pay down the balance.

Read more… Can’t Afford an Emergency Vet Bill? 15 Real Ways Dog Owners Find Help

RedRover Relief and Frankie’s Friends can help with the immediate gap while your appeal is pending — these don’t require your insurance situation to be resolved first.

Read more… 15 Organizations That Help Pay Vet Bills When You Can’t Afford Care

Actionable Next Steps

If you just received a denial letter:

- Read it carefully — identify the exact reason cited

- Call the insurer if the reason is unclear and ask what’s needed to appeal

- Check whether your state is among those with 2026 pet insurance regulations

- Note any appeal deadline mentioned in the letter

If the reason is a pre-existing condition or exclusion you believe is wrong:

- Request a letter from your vet specifically addressing why the current condition is medically distinct

- Gather complete medical records, including from prior veterinarians

- Submit a formal appeal with all documentation

- If denied again and you’re in a regulated state, file a complaint with your state’s Department of Insurance, referencing the relevant law

If the reason is documentation:

- Ask exactly what’s missing

- Resubmit with complete itemized invoices and any requested records

- This category has the highest appeal success rate — don’t assume it’s final

If you need to cover the bill while the appeal is pending:

- Apply for CareCredit or Scratchpay to bridge the gap

- Apply to RedRover Relief or Frankie’s Friends if the bill is substantial

Frequently Asked Questions

Why was my pet insurance claim denied for a pre-existing condition if my dog was never diagnosed?

A formal diagnosis isn’t always required. Many insurers consider symptoms, veterinary notes, or clinical signs that appeared before your policy started or during a waiting period when determining whether a condition is pre-existing. In states that have adopted versions of the NAIC Pet Insurance Model Act, insurers may face stricter standards for supporting these decisions, but the rules vary by state.

What is a bilateral exclusion in pet insurance?

A bilateral exclusion applies when your pet had a condition on one side of the body before coverage began and later develops the same condition on the opposite side. Some insurers treat the second injury as related to the first and may deny coverage. If you believe the injuries are medically unrelated, ask your veterinarian to provide supporting documentation.

How long do I have to appeal a denied pet insurance claim?

Appeal deadlines vary by insurer, so check your denial letter immediately. If no deadline is listed, contact your insurance company as soon as possible. Waiting too long could cause your appeal to be rejected, even if you have strong supporting evidence.

What documents do I need to appeal a pet insurance denial?

Most appeals require your denial letter, complete veterinary medical records, itemized invoices, claim forms, and a letter from your veterinarian explaining why the treatment should be covered. Providing complete documentation gives your appeal the best chance of success.

Can I file a complaint with a government agency if my appeal is denied?

Yes. If your insurer rejects your internal appeal, you can usually file a complaint with your state’s Department of Insurance. The regulator can review whether the insurer followed applicable state insurance laws and claims-handling requirements.

Do new pet insurance regulations apply to existing policies?

It depends on your state’s laws and your policy terms. Some consumer protections apply to policies issued or renewed after new laws take effect, while others may apply more broadly. Check your state’s Department of Insurance for the rules that apply to your policy.

What’s the difference between a waiting period denial and a pre-existing condition denial?

A waiting period denial means the treatment occurred before coverage for that type of claim became active. A pre-existing condition denial means the insurer believes the illness, injury, or its symptoms existed before your coverage started or during the waiting period. Although both can result in denied claims, they’re based on different policy rules.

Disclaimer

Disclaimer: This article is for informational and educational purposes only. Pet insurance regulations vary by state and change frequently — information about 2026 regulatory changes reflects publicly available information as of 2026 and may not apply to your specific state, insurer, or policy. PetInsurePrime does not sell pet insurance and receives no compensation from any insurance provider. This article does not constitute legal advice. For disputes involving denied claims, consult your state’s Department of Insurance or a licensed attorney familiar with insurance law in your state. Always read your full policy documents and contact your insurer directly with questions about your specific coverage.

PetInsurePrime | Independent • Research-Based | Helping US dog owners understand real vet costs and coverage options — without the sales pressure.