Updated: June 2026 | Reading Time: 11 Minutes | Reviewed Sources Best Money, Wallace Law, bankrate, Pawplan

You paid your vet bill. You filed the claim. Then you got that letter.

A denial doesn’t mean the case is closed. Most pet owners don’t know this, but many insurers have a structured appeals process — and you typically have 30 to 60 days from the denial date to use it. Miss that window and you likely forfeit your right to dispute entirely. Best Money

This guide walks through exactly what to do — step by step — from the moment you open that denial letter to the moment you escalate if your insurer won’t budge.

Quick Answer How to Appeal a Denied Pet Insurance Claim

If your pet insurance claim was denied, don’t assume the decision is final. Many pet insurance companies allow policyholders to appeal a denied claim by submitting additional documentation, veterinary records, or correcting claim errors. Review your denial letter carefully, gather supporting evidence, and follow your insurer’s appeal process within the required deadline.

Read more…Why Was My Pet Insurance Claim Denied? 5 Common Reasons (And How to Fix Them)

Table of Contents

Why Claims Get Denied

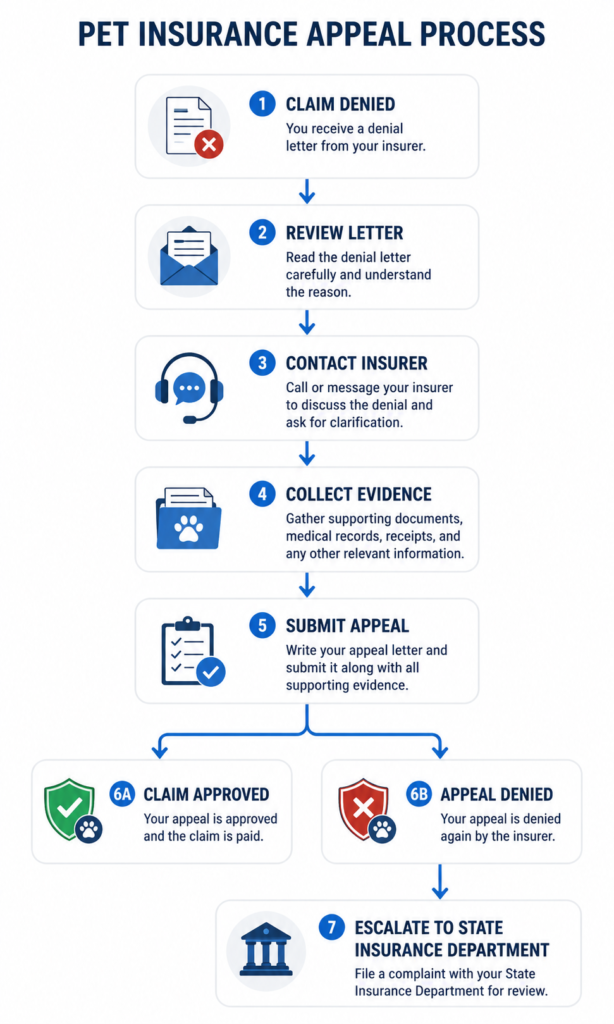

Step 1: Review the Denial Letter

Step 2: Contact Your Insurer

Step 3: Gather Supporting Documents

Step 4: Write an Appeal Letter

Step 5: Follow Up

What If Your Appeal Is Denied?

Common Appeal Mistakes

Frequently Asked Questions

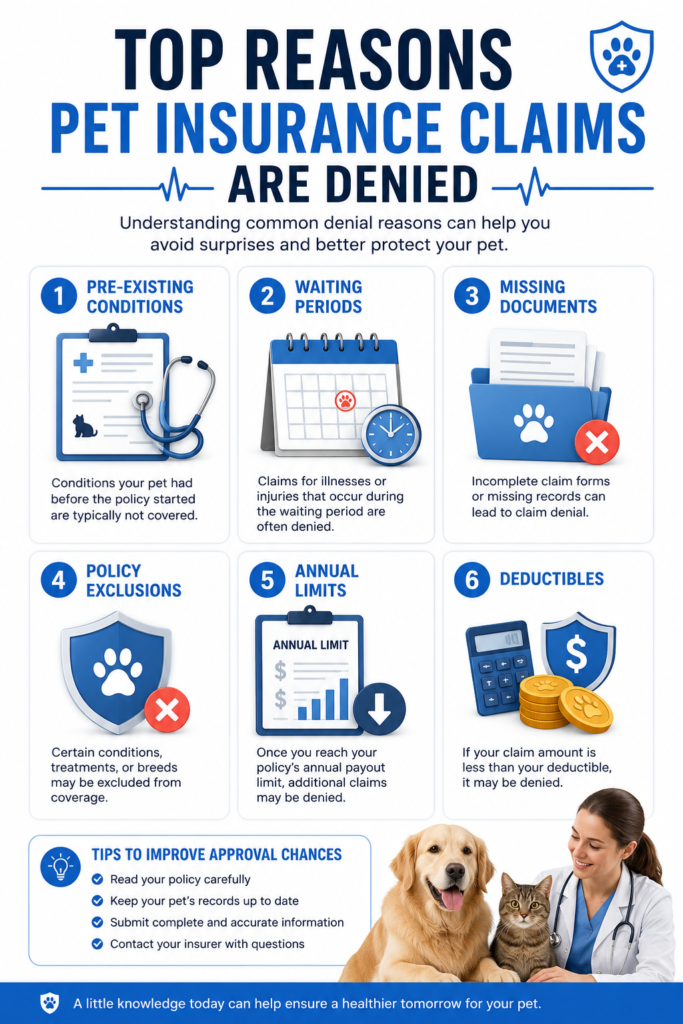

Why Pet Insurance Claims Get Denied

Before you write a single word of an appeal, you need to know why the claim was denied. The reason dictates everything — your strategy, your documents, and your odds.

Typical Pet Insurance Appeal Timeline

| Time | What You Should Do |

|---|---|

| Day 1 | Read the denial letter carefully |

| Day 2 | Contact your insurance company |

| Days 2–5 | Gather veterinary records |

| Week 1 | Submit your appeal |

| Every 7–10 days | Follow up on the appeal |

| If denied again | Request escalation or contact your state insurance department |

The most common reasons:

Pre-existing conditions — This is by far the most frequent denial trigger. Just because an insurance representative says your pet has a pre-existing condition doesn’t automatically make it so. The insurer has the burden of proof — they must have documentation to support that classification. A lot of owners accept this denial without pushing back. Many shouldn’t. Wallace Law

Waiting period violations — Most insurers require claims to be filed within 60–90 days after treatment. Filing outside that window can result in denial even if the treatment would otherwise have been covered. bankrate

Missing or incomplete paperwork — Missing or incorrect information is one of the most common and fixable causes of a denied claim. Sometimes it’s as simple as a missing page from the vet invoice. bankrate

Treatment outside coverage — Routine wellness visits, dental cleanings, preventive care — these are excluded from nearly every standard accident-and-illness plan. If the treatment isn’t covered in your policy, no appeal will change that.

Read more…Dog Surgery Cost in the USA: Real Prices for 2026

Policy limits or deductible timing — The claim may have been processed correctly but denied because you hadn’t yet met your annual deductible, or you’d hit your coverage limit for the year.

This doesn’t always mean the insurer is correct. Sometimes a condition is incorrectly classified as pre-existing because of incomplete medical records or an earlier symptom that may not be related. Review your pet’s medical history carefully before accepting the denial

Read the denial letter closely. Insurers are required to tell you the specific reason. That reason is where you start.

Step 1: Read the Denial Letter Like a Contract

Don’t skim it. The denial letter will reference specific policy sections, exclusion clauses, or timeline violations. Pull out your actual policy document and find every section they cited.

Read more…Pet Insurance for Dogs in the USA: How It Works (2026)

Ask yourself:

- Does their reasoning hold up against what the policy actually says?

- Is the denial based on a pre-existing condition they’ve documented — or just assumed?

- Was there a paperwork error that caused this?

- Is the treatment actually excluded, or are they interpreting the exclusion broadly?

If anything feels off, that’s your opening.

Step 2: Call the Claims Department — Before You Write Anything

Before drafting a formal appeal, call. Ask for a detailed explanation of the denial. This conversation can also give you insight into how their appeals process works and what documents you’ll need to gather. Staying calm and cooperative during this call matters — you’re more likely to get useful information that way. Pawplan

Document the call:

- Date and time

- Name of the representative

- What they said, word for word if possible

Sometimes denials get reversed at this stage because a human reviews what a system flagged automatically. It’s worth the call before escalating to a formal appeal.

Step 3: Gather Your Evidence

This is where most appeals succeed or fail. Your appeal needs to be backed by solid evidence — complete vet records, the itemized invoice, your policy documents, and the original denial letter. Best Money

If the denial was based on a pre-existing condition classification, this is critical: ask your vet to write a letter stating why they believe the denial was unjustified. A professional opinion from the treating veterinarian carries significant weight in the review. Wallace Law

Documents You’ll Need

| Document | Why It Matters |

|---|---|

| Denial Letter | Explains the reason and appeal deadline |

| Veterinary Records | Shows diagnosis timeline |

| Itemized Invoice | Verifies treatment and costs |

| Insurance Policy | Helps cite the correct coverage |

| Vet Support Letter | Strengthens disputed claims |

| Previous Approved Claims | Demonstrates consistency if relevant |

Don’t send originals. Send copies. Keep everything.

Step 4: Write a Clear, Factual Appeal Letter

Keep it short and professional. Emotional appeals don’t move insurance reviewers. Facts and documentation do.

What to include:

- Your name, policy number, claim number, and denial date

- A direct statement that you are formally appealing the decision

- The specific reason the insurer gave for the denial

- Your counter-argument, citing the exact policy language that supports your position

- A list of the supporting documents you’re attaching

- A request for a written decision within a specific timeframe (10–14 business days is reasonable)

Tone: Professional. Not aggressive, not pleading. You’re making a documented case.

Submission: Send your appeal via certified mail with return receipt requested, or through your insurer’s online portal. Keep copies of everything, including the date sent, delivery method, and any confirmation numbers. Best Money

Step 5: Follow Up Consistently

Contact the claims department every 7–10 days to check your appeal status. Document every conversation — date, time, representative’s name, and what was discussed. If the appeal takes longer than the stated timeframe, ask to speak with a supervisor and request a specific decision date. Best Money

Persistence here isn’t optional. Appeals that go quiet often go nowhere.

Step 6: Is It Worth Appealing

| Reason for Denial | Should You Appeal? |

|---|---|

| Missing paperwork | ✅ Yes |

| Incorrect pre-existing condition | ✅ Yes |

| Coding error | ✅ Yes |

| Waiting period dispute | ⚠️ Maybe |

| Annual limit reached | ❌ Usually No |

| Excluded treatment | ❌ Usually No |

What If Your Pet Insurance Appeal Is Denied Again?

This is what most dog owners don’t know about — and it’s often the most powerful move available to them.

Request a Second-Level Review

If your first appeal is denied, you can request a second-level review by a senior claims manager. Most insurance companies have multi-level appeal processes. Ask specifically for this in writing. Best Money

Contact Your State Insurance Department

Read more…15 Organizations That Help Pay Vet Bills When You Can’t Afford Care

Pet insurance companies in the United States are regulated at the state level by each state’s Department of Insurance. These agencies investigate complaints including denied claims, bad faith denials, and delayed processing. JusticeDirect

Many states offer free mediation services or formal complaint processes that investigate claim handling practices. This is a real lever — insurers take state department complaints seriously. MoneyGeek

Most state insurance departments allow consumers to file complaints online, by mail, or by phone. You can find your state’s department through the NAIC (National Association of Insurance Commissioners) website. JusticeDirect

Keep in mind: in states like Washington, the insurer has the burden of proving a pre-existing condition exclusion applies — the law explicitly says so. Check your own state’s regulations. Some offer stronger consumer protections than others. wa

Consider Independent Legal Advice (Only for High-Value Disputes)

While the BBB isn’t a government agency and a complaint there won’t result in legal action, it does affect your insurer’s public reputation and provides useful information to other consumers. Think of it as a secondary pressure tool, not a resolution mechanism. Money

What Actually Happens If Your Appeal Is Approved

If your appeal succeeds, the insurance company processes your claim according to your policy terms and sends reimbursement within 2–4 weeks. You’ll receive an explanation of benefits showing the covered amount, deductible applied, reimbursement percentage, and final payment. Best Money

Common Mistakes to Avoid When Appealing

- Missing the appeal deadline

- Sending incomplete veterinary records

- Not reading the denial reason carefully

- Failing to reference policy language

- Sending original documents instead of copies

- Becoming emotional instead of factual

Read more… Dog MRI Cost in the USA (2026)

What Owners Get Wrong Most Often

Real reviews from policyholders reveal a few consistent mistakes:

Accepting a pre-existing condition label without proof. Insurers sometimes classify new conditions as pre-existing without solid documentation. Push back. Ask them to show exactly which vet record supports their determination.

Waiting too long to appeal. You can appeal within 60 to 90 days of the denial letter, though the exact window varies by insurer. Don’t assume you have unlimited time. Money

Not getting a vet letter. A veterinarian stating in writing that a condition wasn’t present before coverage began can change a denial into an approval. It costs a small records fee. It’s worth it.

Going in combative. Calm, documented, professional appeals get further than angry ones — every time.

One More Thing: Check If Your State Gives You Extra Protection

Pet insurance regulation varies significantly by state. Some states have passed laws requiring insurers to disclose exclusions upfront. Others specifically limit how waiting periods can be applied. If you’re in California, Texas, Washington, or New York, your state insurance department’s consumer protection division may have specific guidance for pet insurance disputes.

A quick search for “[your state] + Department of Insurance + pet insurance complaint” will show you exactly where to file and what protections apply to you.

Pet Insurance Appeal Checklist

✅ Read the denial letter

✅ Contact your insurer

✅ Gather medical records

✅ Get a veterinarian’s written statement

✅ Review your policy wording

✅ Submit your appeal before the deadline

✅ Keep copies of everything

Freqquesntly Asked Questions

Can a pet insurance company deny a claim without giving a reason?

No. Your insurer should explain why the claim was denied in writing, usually in a denial letter. If the explanation is unclear or incomplete, contact the claims department and request a detailed written reason before deciding whether to appeal.

How long does a pet insurance appeal take?

No. Your insurer should explain why the claim was denied in writing, usually in a denial letter. If the explanation is unclear or incomplete, contact the claims department and request a detailed written reason before deciding whether to appeal.

Does appealing a pet insurance claim increase my premium?

Generally, no. Filing an appeal alone doesn’t usually increase your premium. Future premium changes are more commonly based on factors such as your pet’s age, breed, location, or overall pricing changes made by the insurer—not because you challenged a denied claim.

What if my claim was denied because of a pre-existing condition?

Don’t assume the insurer is automatically correct. Ask for the medical records or policy language used to classify the condition as pre-existing. If your veterinarian believes the condition was incorrectly classified, request a written statement to support your appeal.

Can I get legal help if my appeal is denied?

Yes. If you believe your insurer acted unfairly or in bad faith, you may consult an insurance attorney. For many disputes, however, filing a complaint with your state’s Department of Insurance is a practical first step before pursuing legal action.

Can my veterinarian help me appeal a denied pet insurance claim?

Yes. A letter from your veterinarian explaining the diagnosis, treatment, or why a condition shouldn’t be considered pre-existing can strengthen your appeal, especially when medical records support your case.

What documents should I include with my pet insurance appeal?

Include your denial letter, itemized veterinary invoice, medical records, relevant diagnostic reports, a copy of your policy, and any supporting letter from your veterinarian. Complete documentation can improve your chances of a successful review.

Disclaimer

This article is for informational and educational purposes only. Cost data reflects 2026 national averages from NAPHIA, Insurify, and MetLife Pet Insurance and will vary based on your dog’s age, breed, location, and the specific plan you choose. PetInsurePrime does not sell pet insurance and receives no compensation from any insurance provider. Always compare multiple quotes and read your policy documents carefully before enrolling.

PetInsurePrime | Independent • Research-Based | Helping US dog owners understand real vet costs and coverage options — without the sales pressure.